This post was originally published on this site

The rally lifting U.S. stocks to fresh 2023 highs in the year’s home stretch could be at risk if the Federal Reserve next week crushes expectations for interest rate cuts in 2024.

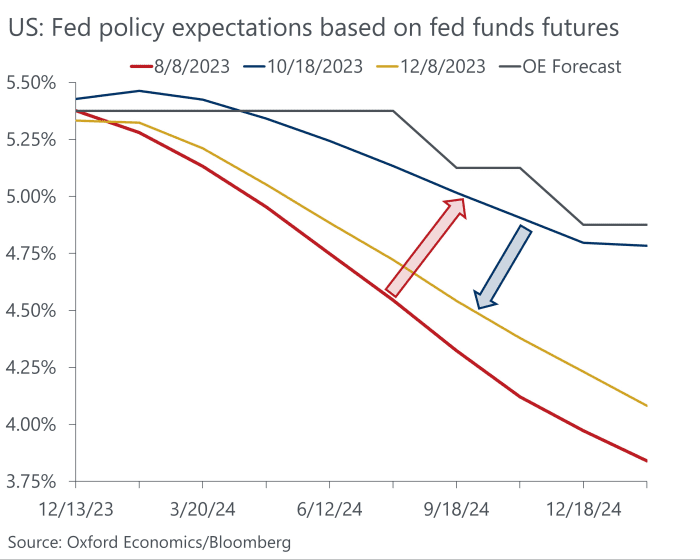

U.S. central bankers and investors haven’t exactly been seeing eye-to-eye about when the Fed will start easing its monetary policy, according to Melissa Brown, senior principal of Applied Research at Axioma.

Traders also have been flip-flopping on their forecasts for rate cuts over the past few months, based on Fed funds futures data.

Oxford Economics/Bloomberg

Given the whipsaw of recent volatility, it isn’t hard to imagine a jittery market backdrop as investors wait to hear from Fed Chairman Jerome Powell next Wednesday, even though the central bank isn’t expected to change its range for short-term interest rates. Since July, the Fed funds rate rate has been unchanged at a 22-year high in a 5.25% to 5.5% range.

U.S. stocks advanced this year after a bruising 2022, adding big gains in November, as benchmark 10-year Treasury yields

BX:TMUBMUSD10Y

tumbled from a 16-year high of 5%. The Dow Jones Industrial Average

DJIA

closed on Friday only 1.5% away from its record close nearly two years ago. The S&P 500 index

SPX

booked its highest finish since March 2022, according to Dow Jones Market Data.

Year Ahead: The VIX says stocks are ‘reliably in a bull market’ heading into 2024. Here’s how to read it.

“I don’t see any report on the horizon that would really make them [the Fed] change their stance on where we are on monetary policy,” said Alex McGrath, chief investment officer at NorthEnd Private Wealth. It is mostly the expectation of Fed rate cuts next year that have supported stock and bond markets rallies recently, he said.

The Dow Jones closed 9.4% higher on the year through Friday, the S&P 500 was up 19.9% and the Nasdaq Composite advanced 37.6% for the same period, according to FactSet data.

“We have been a little skeptical of the market’s excitement over rate cuts early next year,” said Ed Clissold, chief U.S. strategist at Ned Davis Research.

It takes a gradual process for the Fed to move away from its monetary policy tightening, Clissold told MarketWatch. The Fed is likely to pivot its tone from being very hawkish to neutral, remove the tightening bias, and then talk about rate cuts, noted Clissold.

The bond market on Friday already was again flashing signs of a potential rethink by investors about the path of interest rates in 2024.

Junk bonds

JNK

HYG,

often a canary in the coal mine for markets, hit pause on a rally that started in late October as benchmark borrowing costs fell, even though the sector has benefited from big inflows of funds in recent weeks.

Treasury yields for 10-year and 30-year

BX:TMUBMUSD30Y

bonds also shot higher Friday, echoing volatility that took hold in mid-October.

Read: Investors have fought a 2-year battle with the bond market. Here’s what’s next.

Mike Sanders, head of fixed income at Madison Investments, has been similarly cautious. “I think the market is a little too aggressive in terms of thinking that cuts are going to occur in March,” Sanders said. It is more likely that the Fed will start cutting rates in the second half of next year, he said.

“I think the biggest thing is that the continued strength in the labor market continues to make the services inflation stickier,” Sanders said. “Right now we just don’t see the weakness that we need to get that down.”

Friday’s U.S. employment report adds to his concerns. About 199,000 new jobs were created in November, the government said Friday. Economists polled by the Wall Street Journal had forecast 190,000 jobs. The report also showed rising wages and a retreating unemployment rate to a four-month low of 3.7% from 3.9%.

The U.S. central bank next week will likely “try their best to push back on the narrative of cuts coming very soon,” Sanders said. That could be accomplished in its updated “dot plot” interest rate forecast, also due Wednesday, which will provide the Fed’s latest thinking on the likely path of monetary policy. The Fed’s update in September surprised some in the market as it bolstered the central bank’s stance of higher rates for longer.

There’s still a chance that inflation will reaccelerate, Sanders said. “The Fed is worried about the inflation side more than anything else. For them to take the foot off the brake sooner, it just doesn’t do them any good.”

Ahead of the Fed decision, an inflation update is due Tuesday in the November consumer-price index, while the producer-price index is due Wednesday.

Still, seasonality factors could aid the stock market in December. The Dow Jones Industrial Average in December rises about 70% of the time, regardless of whether it is in a bull or bear market, according to historical data.

See: Stock market barrels into year-end with momentum. What that means for December and beyond.

“The overall market outlook remains constructive,” said Ned Davis’s Clissold. “A soft landing scenario could support the bull market continuing.”

Last week the Dow eked out a gain of less than 0.1%, the S&P 500 edged up 0.2% and the Nasdaq rose 0.7%. All three major indexes went up for a sixth straight week, with the Dow logging its longest weekly winning streak since February 2019, according to Dow Jones Market Data.