This post was originally published on this site

Germany’s blue-chip index is a eyeing a fresh record as investors warm to its tech-lite mix of relatively lowly-valued but high quality industrials, carmakers, insurance and healthcare companies.

The DAX

DAX,

which was the DAX 30 until 10 more companies were added in September 2021, at one point on Thursday was up more than 1.5% to sit less than 0.5% from its previous closing high of 16,271.75 hit in early January 2022.

One way for U.S. investors to track German stocks is via the Global X DAX Germany ETF

DAX,

A broader European vehicle is the Vanguard FTSE Europe ETF

VGK,

It’s been a long journey, but the DAX has finally caught back up with Wall Street after underperforming for much of the three years since the COVID-19 pandemic panic struck markets.

Indeed, since the S&P 500 hit its bear market trough in October 2022, as investors fretted about how multi-decade high inflation would cause the Federal Reserve to spike borrowing costs, the DAX 40 has rebounded 35% to the S&P’s 16%.

So, what’s behind this rejuvenation? To simplify, many of the things that were making German stocks seem less attractive are no longer such a drag.

First to consider is the Ukraine war and the concomitant surge in energy costs. The DAX was among the worst global performers in the weeks following Russia’s attack on Ukraine in February 2022 as markets worried about the danger of the war spilling over and the damage to sentiment it caused.

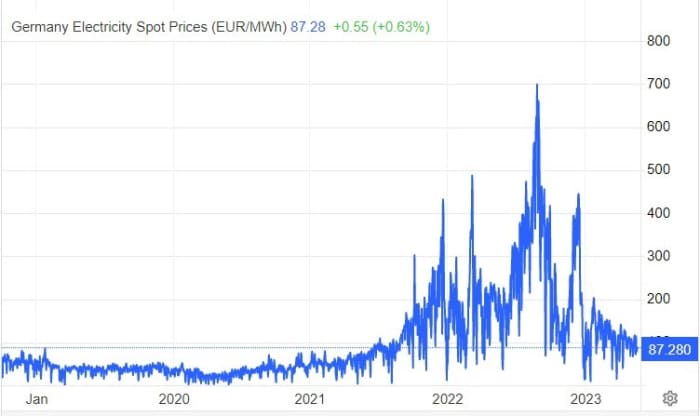

Germany’s energy-intensive industry, and households, were quickly faced with dramatically higher energy prices as natural gas costs soared. Electricity spot prices in Germany rose from around €50 per megawatt-hour at the start of 2021 to nearly €700 in August 2022, according to Trading Economics.

But the apparently successful weaning off Russian supplies has helped push the price down below €90, supporting business sentiment and operating margins.

“Germany was hugely reliant on Russian hydrocarbons so its economy was right in the firing line when sanctions were imposed and prices soared. Clever sourcing of alternative supplies of energy, notably LNG, plus a policy U-turn on coal usage and well-observed campaigns to curb consumption, helped the economy through, as did a mild winter. In sum, the worst case did not happen and stocks that suffered a beating in mid-2022 have rallied,” Russ Mould, AJ Bell investment director told MarketWatch.

Source: Trading Economics.

The second factor helping the DAX is the re-opening of the Chinese economy after Beijing removed COVID-19 restrictions. Data released last month showed the Chinese economy growing by a faster than expected 4.5% in the first quarter, good news for German exporters.

“Germany is an export-driven economy, so hopes for a mild global downturn (at worst) and China’s reopening are also boosting sentiment,” said Mould.

DAX constituents get 23.9% of their total revenue from the U.S. according to FactSet. But the next biggest foreign market is mainland China on 8.4%. And importantly those Chinese revenues are growing faster, up nearly 12% over the past year compared to U.S. growth of just shy of 10%.

In comparison S&P 500 sales to China make up 7.3% of total revenue, but geopolitical and trade tensions mean this has fallen nearly 3% over the past year.

Specialist engineering groups such as Siemens

SIE,

in particular are seen benefiting from China’s economic expansion. And news of increasing consumer spending has helped shares of vehicle manufacturers Mercedes-Benz

MBG,

and BMW

BMW,

up 14.6% and 22.6% so far this year respectively.

Incidentally, the same driver is also behind France’s CAC 40 index hitting a record in April as luxury goods companies like LVMH

MC,

and L’Oréal

OR,

have prospered.

Such tailwinds are attracting more foreign inflows to not just Germany but the continent more broadly. By the end of the first quarter investors had pulled $34 billion from U.S. equities funds so far this year, according to recent data from EPFR.

Europe, in contrast, had seen $10 billion of inflows. BlackRock Investment Institute recently said it expected U.S. equities to underperform stocks in emerging markets, Europe and China over the coming decades.

And yet global investors’ “current allocation is in line with its long-term average,” says Michael Hartnett, investment strategist at Bank of America, citing the latest survey undertaken by the bank.

Source: Bank of America.

Part of the reason for these trends is that over recent months some investors perceived — before A.I. fever again boosted U.S. tech stocks — that what was previously a structural problem for the German market is now an advantage.

In the higher interest rate environment richly valued technology stocks are considered less attractive by some investors. The DAX’s biggest constituent is software group SAP

SAP,

but generally the index is tech-lite, with the sector having a weighting of about 14%, compared to the S&P 500’s 26%.

Indeed, the DAX 40’s sector weightings are more evenly spread, with Automobiles 11.6%, Insurance 11.7%, Industrials 19.2 (including the Siemens suite of companies) Pharma and healthcare 10.6%.

And, perhaps most importantly, the valuation placed on this basket of companies is relatively low. According to Factset, the forward price to earnings ratio for the S&P 500 is 18.0. For the DAX it is 11.4.

Indeed, the geographically broader Euro STOXX 50 trades off a forward p/e of 11.9, leaving the continent as a whole attractive, analysts observe.

European equities “are the winningest geographic segment this year, handily beating U.S. and emerging markets stocks. Even still, recent price action is not especially unusual relative to the historical record. This suggests the current rally is sustainable and could well continue through the balance of Q2 2023,” said Nicholas Colas, co-founder of Datatrek, in a recent note.