This post was originally published on this site

America’s high inflation rate will produce a 7% increase in the size of the standard deduction when workers file their taxes on their 2023 income, according to new inflation adjustments from the Internal Revenue Service.

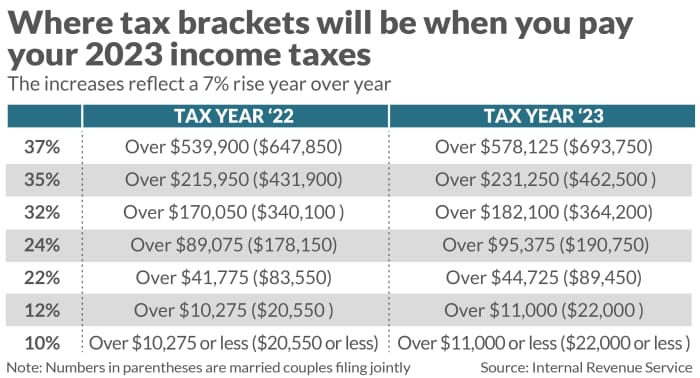

It’s also going to pump up tax brackets by 7% as well, according to the annual inflation adjustments the IRS announced Tuesday.

Many tax code provisions — but not all — are indexed for inflation, so the announcements are a recurring event. But when inflation is persistently clinging to four-decade highs, these annual adjustments carry extra significance.

“When inflation is persistently clinging to four-decade highs, these annual adjustments of approximately 7% for the standard deduction carry extra significance.”

Start with the standard deduction, which is what most people use instead of itemizing deductions.

The standard deduction for individuals and married people filing separately will be $13,850 for the 2023 tax year. That’s a $900 increase from the $12,950 standard deduction for the upcoming tax season.

For married couples filing jointly, the payout climbs to $27,700 for the 2023 tax year. That’s a $1,800 increase from the $25,900 standard deduction set for the upcoming tax year.

The increases in the marginal tax rates reflect the same 7% rise. For example, the 22% tax bracket for this year is over $41,775 for single filers and over $83,550 for married couples filing jointly. Next year, the same 22% bracket applies to incomes over $44,725 and over $89,450 for married couples filing jointly.

MarketWatch/IRS

“The changes seem to be much larger than previous years because inflation is running much higher than it has in previous decades,” said Alex Durante, economist at the Tax Foundation, a right-leaning tax think tank.

The IRS arrives at its inflation adjustments by averaging a slightly different inflation gauge, the so-called “chained Consumer Price Index” instead of the widely-watched Consumer Price Index, Durante noted. That’s an outcome of the Trump-era Tax Cuts and Jobs Act of 2017, he added.

“The reason they do this is because the regular CPI is thought to overstate inflation because it doesn’t take into account the substitution that shoppers can make as cost rise,” Durante said. Shoppers substitute when they swap a more expensive item for cheaper one, and research shows many Americans are using the tactic.

The IRS inflation adjustments come after September CPI data last week showed the yearly rate of inflation at 8.2% in September, slightly off from 8.3% in August. Also last week, the Social Security Administration said next year’s payments would include an 8.7% cost of living adjustment.

“The payout on the earned income tax credit — geared at low- and moderate-income working families who have been hit hard by red-hot inflation — is also increasing. ”

The payout on the earned income tax credit is also increasing. The maximum payout for a qualifying taxpayer with at least three qualifying children climbs to $7,430, up from $6,935 for this tax year. The longstanding credit is geared at low- and moderate-income working families who have been hit hard by red-hot inflation.

More than 60 provisions are slated for an increase inline with inflation, but many portions of the tax code are not indexed for inflation. Depending on the circumstances, the taxes or the tax breaks kick in sooner.

Capital gains tax rules one example. The IRS lets a taxpayer use capital losses to offset capital gains taxes. If losses exceed gains, the IRS allows a taxpayer to deduct up to $3,000 in excess loses. They can then carry the remainder of the capital loses to future tax years. It’s been more than four decades since lawmakers last set the limit, according to Durante.

“While more than 60 provisions are slated for an increase inline with inflation, many portions of the tax code are not indexed for inflation. They include capital gains tax. ”

Given the stock market’s rocky downward slide this year, many investors might welcome a fast-approaching tax break — even if it only enables a $3,000 deduction.

At the same time, a married couple selling their home can exclude the first $500,000 of the sale from capital gains taxation, and it’s $250,000 for a single filer. It’s been that way since the exclusion’s 1997 establishment.

The once white-hot housing market may be cooling, but many sellers may still be facing the point when taxes kick in. The median home listing was over $367,000 as of early October, according to Redfin

RDFN,

The child tax credit is another example. After the payout to parents last year jumped to $3,600 for children under age 6 and $3,000 per child age 6 to 17, it’s back to a maximum $2,000. The credit’s refundable portion climbs from $1,500 to $1,600 during tax year 2023, the IRS notes.

Proponents of the boosted payouts and some Congressional Democrats want to revive the larger payments in negotiations tied to corporate taxes. The high costs of living are a strong reason to bring back the boosted credit, they say.