This post was originally published on this site

Hello and welcome to Financial Face-off, a MarketWatch column where we help you weigh financial decisions. Our columnist will give her verdict. Tell us in the comments whether you think she’s right, and please send in suggestions for future Financial Face-off columns.

The face-off

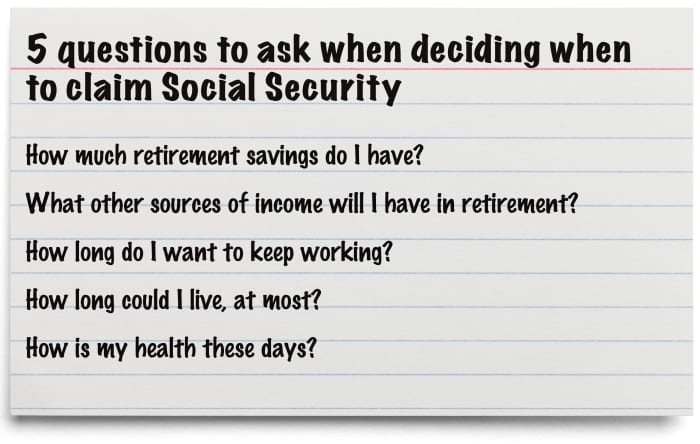

Almost everyone who’s had a paid job in the U.S. is eligible to receive Social Security benefits when they retire. What some people may not realize is that they get to decide when they start receiving those monthly payments. You can become eligible for Social Security retirement benefits as early as age 62, or 60 if you’re a widow or widower. The question is: Should you claim your Social Security retirement benefits earlier or later?

What’s at stake?

The longer you wait to collect your benefits, the more money you’ll get, until hitting the highest possible benefit at 70. Your benefit goes up every single month that you wait between age 62 and 70, around 7% or 8% a year.

At age 70, your benefit is about 76% higher than what it would have been at age 62, said Martha Shedden, a retired civil engineer who became so passionate about the need to educate people about Social Security that she co-founded the National Association of Registered Social Security Analysts, a group that trains people as Social Security counselors.

Before deciding when to start collecting, figure out the difference between what your benefit would be earlier vs. later, Shedden said. Seeing that number helps people understand that the timing question is “a very very serious financial decision,” Shedden said.

This handy calculator will estimate your personal benefits and tell you how much you would get if you start claiming at age 62, 67 or 70. Someone who was born in 1960 and has an average annual income of $50,000 would get $1,338 per month at age 62; $1,911 at their full retirement age (67); or $2,370 at age 70, according to an AARP calculator. You should also make an account on the Social Security Administration’s website, which will give you an estimate of your benefit at various intervals.

The average Social Security payment is currently $1,660. The earlier you start, the longer you’ll receive those benefits. But you’ll be receiving the permanently reduced amount (plus modest cost of living adjustments) for the rest of your life. If you wait until your full retirement age (which is set by the government and depends on your birth year), you can receive the full Social Security benefit.

At full retirement age, you can earn additional income, from a part-time job, for example, and your Social Security benefits won’t be reduced. (Before full retirement age, benefits shrink if you earn over a certain amount of income from other sources.) At age 70, the benefits max out.

In previous generations, people tended to start collecting Social Security at age 62 because they assumed that’s what they were supposed to do, Shedden said. But there’s been growing awareness in recent years about the value of waiting.

A key question to ask yourself: How long do you want to work? Some people love their jobs; others can’t wait to get out of the workplace. If you keep working while you’re receiving Social Security, you run the risk of earning too much income, which can reduce your benefits. (However, you will get that money back in the form of larger monthly payments once you hit full retirement age.)

Once you’ve claimed Social Security benefits, you have a 12-month window during which you’re allowed to change your mind and stop receiving benefits — but you’ll have to pay back the amount you’ve received so far.

You’ll also need to consider your health, both physical and financial. People who don’t have enough retirement savings often have no choice but to take Social Security as soon as they can. (About half of the 65+ population gets at least half of their family income from Social Security; 25% of older households rely on it for at least 90% of their income.)

If your family history suggests you’re going to live into your 90s, you may want to try waiting to collect if possible so you can get the most amount of money. But there’s also a balance. If you were to begin claiming Social Security at your full retirement age, you would receive the full amount of benefits you’re owed. Anyone who claims before their FRA receives a permanent reduction of that amount, but could also balance those benefit checks with lower withdrawals from their retirement savings, giving those accounts the ability to continue to grow over time.

People should think in terms of how long they could live at maximum, not average lifespan, Shedden said. “We generally underestimate how long we’re going to live and by doing that we can have ‘longevity risk,’ which is the risk of running out of money later in life,” Shedden said.

It’s also important to think about the other players in the equation. Divorced spouses, deceased spouses, current spouses, young children and adult children with disabilities can all factor into your Social Security benefits. “It’s a family decision,” Shedden said.

Another issue that comes up in conversations about Social Security: Some people think they should start collecting as soon as possible because they’re worried the government will “run out of money.” That’s not going to happen, and that’s not a reason to claim earlier, said financial advisers interviewed by MarketWatch.

Deciding when to claim Social Security can be an emotional discussion for people because it touches on core fears about the end of our lives and whether we’ll have enough money to care for ourselves. But once people decide, they’re so relieved, said Shedden. It’s a central decision, and after it’s made, other retirement planning can proceed more easily.

My verdict

Wait — if you’re lucky enough to be among the Americans with sufficient retirement savings and good health. (Some 26% of Americans who are still working have no retirement savings, according to the latest Federal Reserve report on U.S. households’ economic well-being. Of those that have savings, only 36% think their retirement savings are “on track.”)

My reasons

The huge difference between what your monthly payment will be at age 62 vs. age 70 convinced me. I’d also like to think that if you plan for a long and healthy life, you’ll increase your chances of having one, but maybe that’s the optimist in me talking.

On the other hand

One argument in favor of claiming your Social Security benefits earlier: you may lose your chance to enjoy the extra money if you wait too long to claim your benefits. If you’ll have to scrimp and save to support yourself while you wait until full benefits kick in at 70, your quality of life and satisfaction may suffer, said Grant Meyer, a certified financial planner and founder of GTS Financial in Bloomington, Minn.

At 62 or 65, even though your Social Security benefit would be smaller, the extra money could still help you take a vacation, spend time with your grandchildren, or get out of a job you hate, Meyer said. By the time you’re eligible for the full benefit, you may be less mobile and less healthy.

“You need to understand your entire financial picture, but some people forget about quality of life and satisfaction,” Meyer said. “It’s easy to forget those because they aren’t numbers that show up on a spreadsheet, but they’re something to think about when you walk through Social Security.”

Another argument for taking Social Security money earlier is that it can help people avoid spending their retirement investments on daily expenses, which allows retirement savings to keep growing, said Joseph Favorito, managing partner at Landmark Wealth Management in Melville, N.Y. Favorito generally favors collecting Social Security earlier. But by his calculations, a 5% compounded return on investments would outpace the annual 8% simple interest increase on Social Security.

“If I take that dollar amount that I didn’t spend because I had my Social Security benefit at 62 and I kept it and invested it, and I do live to 95 or 100, even though I might have collected less from Social Security, the amount of money that accumulated, that stayed invested over that time, far outpaces by a large number what I would have otherwise gotten from Social Security with those higher payments,” Favorito said. However, that strategy only works for people who are disciplined investors who don’t panic during periods of volatility, he said.

Tell us in the comments which option should win in this Financial Face-off and let us know your questions for future Financial Face-off columns.