This post was originally published on this site

Meet the force behind TINA — the popular trader acronym for the notion that “there is no alternative” to stocks.

Real, or inflation-adjusted, yields on safe government bonds have remained persistently negative despite rising inflation, contributing to continued demand by return-hungry investors for stocks and other assets perceived as risky.

The concept is simple. “The more real yields fall, the better other assets look in comparison” to bonds, said Joe Kalish, chief global macro strategist at Ned Davis Research, in a phone interview.

And they have certainly fallen. The real yield on 10-year U.S. Treasury inflation-protected securities, or TIPS, hit an all-time low of -1.196%, based on data going back to 2003, on Nov. 9 and hasn’t moved far off that level since, according to Tradeweb, ending Friday at -1.136%.

The phenomenon, in the face of rising inflation pressures, has presented something of a head scratcher for investors and analysts. Kalish previously dubbed negative real yields “the biggest puzzle in fixed income.”

The strategist put some of those puzzle pieces together in a Nov. 16 note, identifying three main drivers behind negative yields:

- Investors looking for inflation protection have piled into TIPS. After all, TIPS are the only way for investors to directly hedge against inflation, as their principal amount automatically adjusts in line with CPI inflation. The Federal Reserve, of course, is also a buyer of Treasurys, helping to keep a lid on nominal yields.

- At the same time, the Fed has also been snapping up supplies of the inflation protected securities. The central bank holds 22% of all TIPS outstanding.

- Unrelenting demand for Treasurys from foreign buyers is keeping a lid on nominal yields despite rising inflation. U.S. nominal yields remain well above those for bonds in Europe, the U.K. and Japan. U.S. debt looks more attractive even after hedging for currency risk.

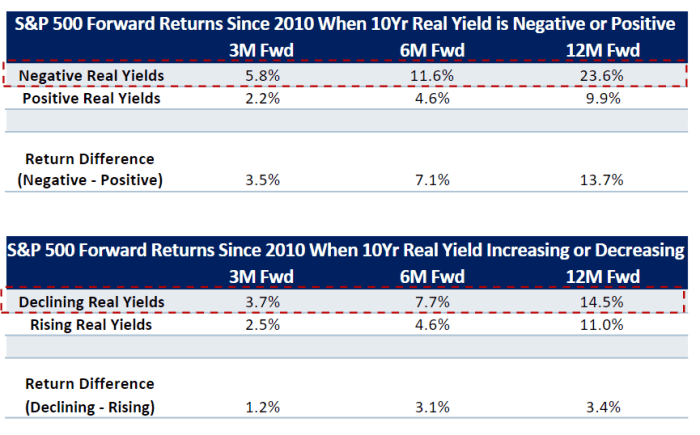

Negative and falling yields have certainly been accompanied by rising equity valuations and strong returns.

In a Nov. 1 note, Lori Calvasina, equity analyst at RBC Capital Markets, took a look at the performance of the S&P 500 stock index

SPX,

since the financial crisis of 2008, tracking it against real yields.

“On a 3-, 6-, and 12-month forward basis, equity market returns have been much stronger when real yields are falling and negative than when they are rising and positive,” Calvasina said (see chart below).

RBC Capital Markets

“This also helps explain, in our opinion, why the U.S. equity market has been more resilient than some have expected of late in the face of what feels like a relentlessly negative news flow.”

Kalish took a look at the forward earnings yields of companies in the S&P 500 and the technology heavy Nasdaq-100

NDX,

plotting them against real 10-year Treasury yields. He found a rising spread resulted in stocks outperforming their historical return, while a falling spread resulted in underperformance. Falling real yields would widen the spread, while rising real yields would narrow it.

The difference in the annual gain for the S&P 500 was around 4 percentage points, he said, and nearly 6 percentage points for the Nasdaq-100.

Indeed, the relationship between real yields and tech stocks is particularly strong, Kalish said, and has strengthened since the Fed pivoted to an easier monetary policy stance in 2019. Tech and other growth-oriented stocks are sensitive to movements in interest rates because their valuations are based on expectations for earnings growth and cash flow.

That means tech stocks and growth-oriented names could be particularly vulnerable if real yields begin to rise, Kalish said.

On the flip side, an index of broad cyclical stocks tends to be positively correlated to real yields — rising and falling together, the analyst noted.

Outside of equities, the inverse relationship between gold and real yields also stands out, with the yellow metal rising when real yields fall and declining when real yields rise.

“Since the GFC (great financial crisis), it seems like just the direction of real yields is what’s mattered for gold,” he said.

And then there’s bitcoin

BTCUSD,

which struggled from its late 2017 peak to late 2018 — a period that was largely accompanied by rising real yields, Kalish noted. He found that bitcoin has rallied 180% per annum when real yields are falling compared with a still quite respectable but much lower — by several orders of magnitude — 37% when real yields are on the rise.

It all speaks to the attention investors need to pay to the Fed and other central banks. The Fed begins tapering its monthly bond purchases this week, on a timetable to wind down the program by June.

Investors have increased bets that the Fed will move quickly to begin raising their policy interest rates once the taper is completed. A flattening of the yield curve as short-term rates rise faster than longer-dated rates in anticipation of Fed action has some investors citing the potential for a policy mistake, with a monetary policy tightening sparking an economic downturn.

Kalish contends the curve is sending a more benign signal, reflecting expectations that the Fed will move in time to rein in inflation. There would be a danger, however, if the Fed ends up delaying its timetable.

“If the Fed and other central banks were to hike rates and start pushing real yields higher it could provide some headwinds to some of these other asset classes,” Kalish said.

Investors will parse the minutes of the Fed’s Nov. 2-3 policy meeting, when they’re released at 2 p.m. Eastern on Wednesday this coming week, a jam-packed day of U.S. data that will also include weekly jobless claims, October durable-goods orders, personal consumption and spending data and other releases ahead of Thanksgiving Day holiday on Thursday, when U.S. markets will be closed.

The Nasdaq Composite

COMP,

closed at a record 16,057.44 on Friday, rising 1.2% for the week. The Dow Jones Industrial Average

DJIA,

suffered a second straight weekly loss, down 1.4%, while the S&P 500 lost 0.3%. The Dow sits 2.4% below its record close from Nov. 8, while the S&P 500 is just 0.4% off its record finish from Thursday.