This post was originally published on this site

Investors may be taking the wrong lessons from the 1970s.

It’s hardly a fond memory, but surging prices in the U.S. and other countries this year have investors and pundits banking on a rerun of 1970s-era “stagflation” — a demoralizing combination of stagnant economic growth and high inflation. The comparisons are understandable, but superficial, offering little insight into what’s actually happening below the surface, said Jean Boivin, head of the BlackRock Investment Institute, in a phone interview.

Why understandable? “We haven’t seen an environment where inflation was mostly driven by supply shocks since the 1970s,” said Boivin, a former Bank of Canada deputy governor. But that’s largely where the comparisons end.

Inflation in the 1970s was amplified by oil embargoes that sent energy prices soaring, slowing the economy and feeding inflation. In the current case, the supply shocks are in large part the result of a demand surge tied to the restart of the global economy after the COVID-19 shutdown. That’s an important difference.

Mirror opposites

In fact, the 1970s and the current situation are opposites in important ways, Boivin said. The stagflation of half a century ago came as growth and activity exceeded the global economy’s productive capacity. Now, the economy is running up against supply-chain bottlenecks, which isn’t the same thing. In fact, the economy is still operating below its productive capacity, he said.

That means supply will eventually rise to meet demand, he said, instead of the 1970s experience of demand going down to meet supply.

And while both episodes share soaring oil prices, the story in the 1970s was one in which the oil supply shutdowns by producers slowed the economy and eroded its operating capacity. Energy prices are jumping now because the economy has restarted, “and there’s no way to restart without energy,” Boivin said. “The causality runs the other way.”

‘Inflationary boom’

Other economists have made similar points.

“To be in stagflation, the economy needs by definition to be stagnating, and the evidence for this is quite thin,” said Neil Dutta, head of U.S. economics at Renaissance Macro Research, in an Oct. 18 note. “By all accounts, the economy remains firmly in boom mode.”

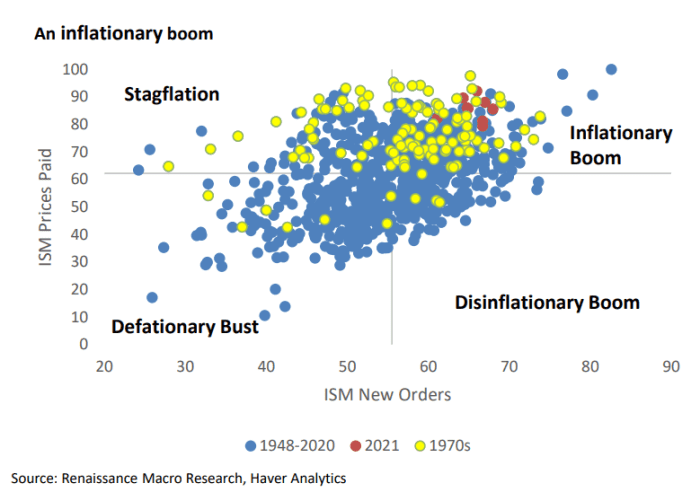

To detect signs of stagflation, Dutta used the Institute for Supply Management’s new orders and prices paid indexes.

On one axis, he put new orders, which serve as a proxy for the demand side of the equation, or how much customers are buying. On the other, he put prices paid, a proxy for inflation. (See chart below).

Renaissance Macro Research

For the economy to be in stagflation, new orders must be below their long-run average — reflecting weak demand from customers — while prices paid

run above its long-run average — meaning inflation is high, Dutta explained. Instead, as shown by the red dots representing 2021 monthly readings, the economy is in an “inflationary boom,” he said, with new orders and prices both strong.

And then theres’ the labor market. Indeed, part of what put the “stag” in the stagflation of the 1970s was the high unemployment that accompanied rising prices.

“At 4.8% today, the unemployment rate is below its 5-, 10-, 15-, 20-, 25-year averages (and so on; you get the picture),” wrote Ross Mayfield, investment strategy analyst at Baird, in a Monday note.

“While the economy is still a few million jobs shy of pre-COVID, the number of job openings is at records and quit rates are soaring,” he said.

Policy mistake ahead?

That doesn’t mean inflation isn’t a concern. And rising inflation expectations, a key metric watched by central bankers, could become a problem. Boivin worries that some policy makers will be too quick and aggressive in responding to inflation increases that monetary policy is ill-equipped to address.

That would risk needlessly destroying demand when what is wanted is bottlenecks to resolve themselves and supply to come back, said the former monetary policy maker. After all, tightening monetary policy would do little to unclog port or fix shortages of semiconductors that have snarled supply chains.

Traders have pulled forward expectations for interest-rate increases and stoking fears that central banks, including the Federal Reserve, will slam on the brakes more aggressively than previously expected, risking an economic downturn.

High-profile investors, including hedge-fund titans Paul Tudor Jones and David Einhorn, have argued that Fed policy makers are inflation creators rather than inflation fighters. And Jack Dorsey, chief executive of Twitter Inc.

TWTR,

and Square Inc.

SQ,

late Friday warned that “hyperinflation” was coming to the U.S. and global economy.

Read: Cathie Wood says Jack Dorsey’s ‘hyperinflation’ call is off the mark

Major stock-market indexes have continued to power higher after stumbling in September as stagflation fears mounted. Investors have wrestled with how to trade inflation as the economy reopens, gauging the role of equities as an inflation hedge versus fears of a rerun of the stagflation scenario.

Equities struggled to keep up with inflation between 1969 and 1982, noted Nicholas Colas, co-founder of DataTrek Research, earlier this year, posting a compounded annual growth rate of negative 0.8% as the economy and the labor market were rocked by rising prices.

Archive: ‘Good’ inflation or ‘bad’? Investors are scared because they can’t tell difference just yet

The S&P 500

SPX,

and Dow Jones Industrial Average

DJIA,

both ended at records on Monday, with the S&P 500 up more than 21% so far in 2021 and the blue-chip gauge up nearly 17%.

Not ‘automatically’ bad for equities

So how long will inflation pressures persist? Anyone making projections should do so with a large sense of humility given the largely unprecedented nature of the post-pandemic restart, Boivin prefaced, saying it would be reasonable to expect high inflation to persist through the first half and perhaps into the second half of 2022.

It’s more important, he said, to recognize the “nature” of the current inflation rise than the time frame. Inflation is likely to remain well above target in 2022 and will remain above target, on average, over the next five years, Boivin said.

For investors, that’s not a bond-friendly environment, he said, with the BlackRock Investment Institute favoring inflation-protected securities over nominal bonds. It’s not an environment that’s “automatically” bad for equities or other risk assets however, “which leaves us net-net underweight government bonds but overweight global equities” as investors see some inflation with a muted policy response.