This post was originally published on this site

https://images.mktw.net/im-217724The Bank of England on Thursday is expected to follow the European Central Bank last week and the Federal Reserve on Wednesday in leaving interest rates unchanged.

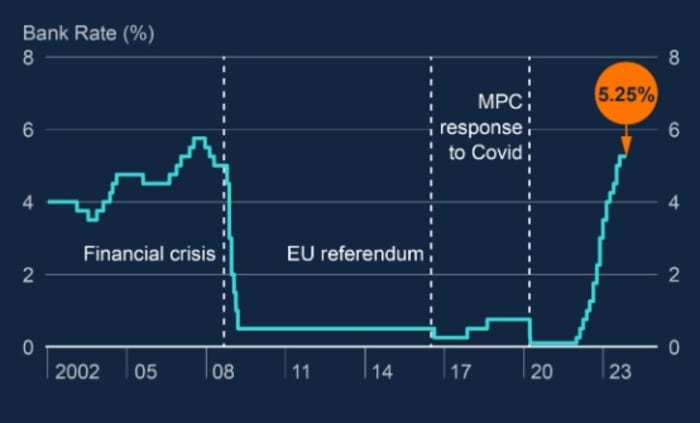

The Bank Rate will remain at 5.25%, the highest since March 2008, for the fourth meeting in a row, according to bets in futures markets.

Consequently, traders will be focusing on what the BoE’s Monetary Policy Committee says in its accompanying statement and economic projections as a guide to when rate cuts may begin.

Source: Bank of England

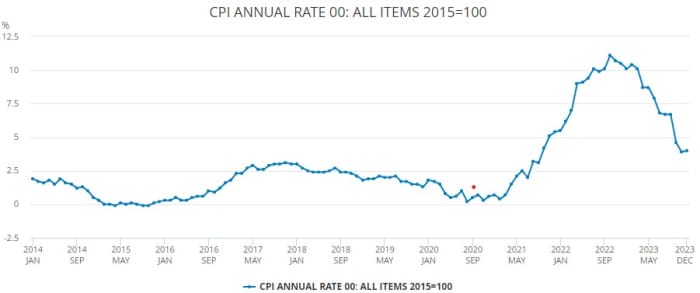

Like it’s U.S. and eurozone peers, the Old Lady of Threadneedle Street has been in a battle with inflation in recent years, delivering 14 interest rate hikes in response to annual consumer price increases that topped 11% in October 2022, amid a surge in energy costs and COVID-related supply disruptions.

Headline CPI inflation has come down sharply since then, touching 4% in December. But that was an uptick from the 3.9% in November, and it remains double the BoE’s 2% target.

Source: Office for National Statistics

Such a scenario might encourage the central bank to maintain a hawkish bias were it not for the poor health of the U.K. economy.

In its November Monetary Policy Report, the MPC said it expected GDP growth to be “broadly flat” in the fourth quarter of 2023, and over coming quarters. It was most likely CPI inflation would return to the 2% target by 2025, it said.

But recent data has been worse than the BoE expected, notes Sanjay Raja, senior economist at Deutsche Bank.

“Since the November MPR, the BoE has been met with one downside surprise after another. Put simply, GDP, wage growth, and inflation have all tracked below the MPC’s November forecasts,” says Raja.

However, this scenario has caused a fall in bond yields and the pricing in of a faster pace of interest rate cuts in coming years, which then may lift growth over the longer term by more than previously expected.

Consequently, the MPC is likely to maintain its poor assessment of 2024 but increase its economic growth forecasts for the next few years, says Goldman Sachs analyst Ibrahim Quadri.

“We expect the growth projections in 2025 and 2026 to be revised up, reflecting the updated conditioning path for Bank Rate, which is down by around 85 basis points, on average, over the forecast horizon, since the November MPR,” said Goldman.

Crucially, Goldman also thinks the BoE will revise down its near-term inflation forecasts because of softer consumption data and lower energy prices, with 2% CPI hit by the end of this year — and this may allow for rates to be cut by the spring.

“[W]e continue to expect the first 25bp cut in May, followed by 25bp cuts every meeting until Bank Rate reaches 3% in May 2025. An earlier cut in March can not be ruled out entirely, especially if the disinflation process is coupled with further deterioration in growth.,” says Goldman.

Sam Cartwright, economist at Societe Generale, agrees: “The magnitude of decline in both pay growth and inflation has reinforced our view of a May cut.”

However, he is wary that because the effect of the National Living Wage increase on pay growth won’t become apparent until after the May meeting, it may encourage the BoE to wait a bit longer.

Still, all told, unless their is another inflation shock, markets should soon get the the easing of policy on which they are betting.

According to interest rate futures trading on ICE, the Bank Rate is indicated to be down to 4.4% by December 2024 and 3.45% a year later.

“[H]aving previously maintained a tightening bias in its forward guidance, the MPC statement should certainly drop its rate-hike bias and acknowledge that, if inflation follows the path assumed in its projection, the next move in rates is likely to be down,” said Daiwa Capital Markets.