This post was originally published on this site

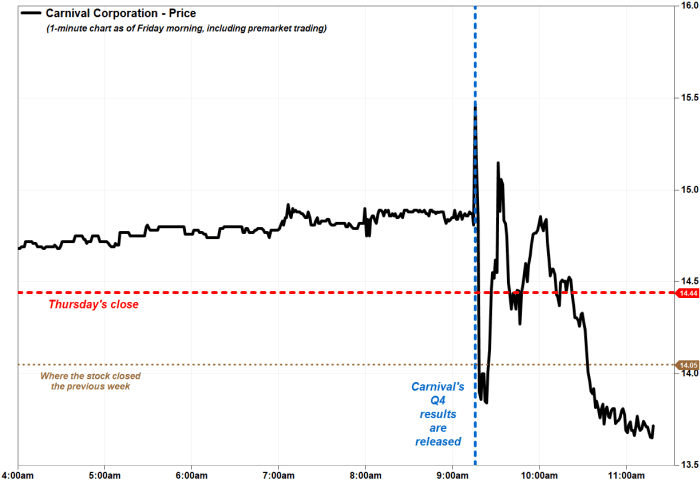

Shares of Carnival Corp. fell in choppy trading after the cruise operator booked its first quarterly profit since before the COVID pandemic, as “significantly elevated” demand led to record revenue and bookings, but provided a downbeat outlook.

The stock

CCL,

CCL,

had swung between gains and losses earlier in the session, before it committed to a sharp loss. It slumped 5.1% in recent morning trading toward a 3 1/2-month low, to put it on track to suffer a fifth-straight weekly loss.

Carnival’s stock falls in choppy trading after earnings report.

FactSet, MarketWatch

The company swung to fiscal third-quarter net income for the quarter to Aug. 31 of $1.07 billion, or 79 cents a share, from a loss of $770 million, or 65 cents a share, in the same period a year ago.

Excluding nonrecurring items, adjusted earnings per share for the quarter to Aug. 31 of 86 cents, which compared with a per-share loss of 58 cents last year, beat the FactSet consensus of 75 cents.

The company had not reported a net profit since the quarter that ended in November 2019, according to FactSet data, while the adjusted profit was the first since the quarter that ended February 2020. (COVID was declared a pandemic on March 11, 2020.)

Revenue grew 59.2% to $6.85 billion, above the FactSet consensus of $6.71 billion, as passenger ticket revenue rose 75.2% to $4.55 billion and onboard and other revenue increased 34.9% to $2.31 billion.

“The outperformance was driven by strength in demand, with both our North America and Australia segment and Europe segment equally outperforming expectations,” said Chief Executive Josh Weinstein.

Booking volumes continued at “significantly elevated levels,” Carnival said, as the company set a new third-quarter record for total bookings that were running nearly 20% above 2019 levels.

“We are maintaining strong momentum and continuing to build demand through our improved commercial execution,” CEO Weinstein said.

For the fourth quarter, however, the company said it expects an adjusted per-share loss of 18 cents to 10 cents, wider than the current FactSet loss consensus of 8 cents a share.

And the company expects earnings before interest, taxes, depreciation and amortization (Ebitda) — what companies use as a measure of underlying profitability — of $800 million to $900 million, below the FactSet consensus of $950 million.

For the company’s fiscal 2023 outlook, the guidance range for adjusted Ebitda was revised lower to $4.10 billion to $4.20 billion from $4.10 billion to $4.25 billion.

And the outlook for growth in adjusted cruise costs excluding fuel, compared with 2019 levels, was raised to approximately 9.5% from prior guidance of 8% to 9%.

The stock has tumbled 13.8% amid its current five-week losing streak, which would be the longest such stretch since the five-week streak that ended May 20, 2022.

It has plunged 20.1% over the past three months but has soared 70.1% year to date. In comparison, the S&P 500 index

SPX

has slipped 1.8% in the past three months, but has gained 12.5% this year.