This post was originally published on this site

By Sept. 30, nearly 55 million Medicare beneficiaries enrolled in Part D prescription drug plans and all types of Medicare Advantage plans will an Annual Notice of Change (ANOC) in their mailbox.

The ANOC outlines the details of your 2023 plan and any changes in benefits or coverage, medical and prescription drugs costs, provider and pharmacy networks, the area you must live in for the plan to accept you as a member, administrative changes and more that will be effective starting in January 2024. “It is important to note that this is a requirement,” said Jae Oh, author of “Maximize Your Medicare.”

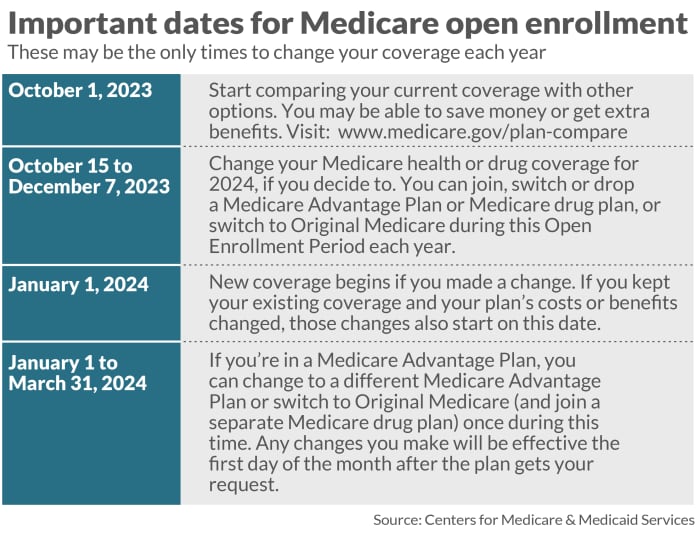

And it’s not a document to be tossed into the circular filing cabinet. Nor is it a document that you should procrastinate reviewing, especially since the annual enrollment period (AEP), that time of year from Oct. 15 to Dec. 7 when Medicare beneficiaries can switch into a plan that might be better suited for them, is just around the corner.

“The most crucial step regarding the Medicare annual notice of change is to read it and not ignore it,” said Katy Votava, president of Goodcare.com and author of “Making the Most of Medicare: A Guide for Baby Boomers.”

Others agree. “The ANOC is a good reminder that plans change from one year to the next,” said Tricia Neuman, senior vice president, executive director for program on Medicare policy and senior adviser to the president at KFF, a nonprofit organization focused on health policy and formerly known as the Kaiser Family Foundation.

In fact, it’s essential to review the ANOC even if you’re satisfied with your current plan. “You should review all your coverage options even if you are happy with your current coverage because plans change their costs and benefits every year,” said Mitchell Clark, director of digital strategy and communications at the Medicare Rights Center, a nonprofit consumer service organization.

Where to start? Medicare Advantage enrollees should review the checklist provided in the beginning pages of the ANOC document to help them decide whether they want to change their plan, said a Centers for Medicare & Medicaid Services (CMS) spokesperson.

Here’s what to review in your ANOC:

Premium and cost changes

The ANOC will outline any increases in monthly premiums, deductibles, copays, and coinsurance. Determine whether any of these costs are rising, and by what amount. Also, consider how these changes might affect your yearly total expenses.

Provider and pharmacy network changes

Review whether your preferred doctors, specialists, hospitals, pharmacies, etc. are still in-network.

“If you have a Medicare Advantage plan, verify with your healthcare providers if they’ll be participating in the plan next year,” advises Votava. “If they aren’t, you’ll need to determine whether to switch providers or seek a plan that better aligns with your needs.”

Medicare beneficiaries enrolled in Part D plans want to be very careful with “preferred pharmacies. “There are still many expensive medications where the copays, deductibles, the coinsurance can be different and notably different in financial terms, meaning a thousand dollars a year for those people with expensive medications,” Oh said.

He also noted that there could be substantial differences in costs for the same prescription drug at preferred pharmacies in a beneficiary’s Part D plan. “You would think that two preferred pharmacies would give you the same price,” he said. “That is not necessarily true.”

Drug coverage/formulary changes

Check if your prescription drugs remain covered. Also, see whether any have shifted to a higher tier, resulting in higher costs at the pharmacy, or if they now require prior authorization—meaning you need special approval to fill certain prescriptions. And review whether you need to switch medications due to formulary changes.

Review any changes in your coverage for the upcoming year. Consider not just the premium cost, but also which medications are covered and their respective copayment levels. “By examining the notice immediately upon receipt, you’ll have ample opportunity to explore alternative coverage options,” Votava said.

Log into your MyMedicare.gov account and update your medication list. “Then that list can auto-populate in medicare.gov, making your shopping less time-consuming and more accurate,” she said.

Also review how some of the provisions in the Inflation Reduction Act of 2022 will affect your 2024 prescription drug costs. These changes include a cap on out-of-pocket drug spending for enrollees in Medicare Part D plans and requiring Part D plans and drug manufacturers to pay a greater share of costs for Part D enrollees with high drug costs, according to a blog post by KFF’s Neuman and a co-author.

“The most notable change will be the end of the catastrophic stage of prescription drug coverage under Part D,” said Oh. “Part D calculations are very, almost crazily complicated.”

According to Neuman’s blog, in 2024, once Part D enrollees without low-income subsidies have drug spending high enough to qualify for catastrophic coverage, they will no longer be required to pay 5% of their drug costs, which in effect means that out-of-pocket spending for Part D enrollees will be capped. In 2024, the catastrophic threshold will be set at $8,000.

“The fact is that once you hit the maximum of $8,000, according to the Medicare definition, your out-of-pocket expense will be much lower than that,” Oh said. “Once you hit $8,000, you’ll not be responsible for any further prescription drug costs under Part D, including prescription drug benefits inside a Medicare Advantage plan.”

Managed care changes

Check whether you will need referrals from your primary care physician (PCP) to see specialists when previously you did not. And determine whether your plan could require you to try cheaper treatments first before approving more expensive options.

Evidence of coverage

If you’re in a Medicare Advantage plan, you’ll receive from your plan alongside your ANOC something called Evidence of Coverage (EOC). The EOC gives you details about what the plan covers, how much you pay, and more in the next year. Your plan will send you a notice (or printed copy) by Oct. 15, which will include information on how to access the EOC electronically or request a printed copy, according to the Medicare & You 2024 Handbook.

If you don’t get your ANOC and EOC in early fall, contact your plan.

Clark also mentions that some plans may send the EOC via email instead of a physical mail. If you prefer a printed version, simply contact your plan to request one.

Who doesn’t receive an ANOC?

New enrollees whose Medicare Advantage plan begins Jan. 1, 2024, will not receive an ANOC, according to a Medicare spokesman.

Likewise, beneficiaries who have purchased a Medicare Supplement Insurance (Medigap) plan will not receive an ANOC. Medigap plans are administered by the states, the CMS spokesperson said. There are standardized federal minimum benefits and they do not change from year to year.

Medigap is extra insurance you can buy from a private health insurance company to help pay your share of out-of-pocket costs, according to Medicare.gov. There are 10 different types of Medigap plans offered in most states, which are named by letters: A-D, F, G, and K-N. Price is the only difference between plans with the same letter that are sold by different insurance companies, according to Medicare.gov.

Oh noted Medigap plan providers do notify policyholders of premium changes. “But there is no definition to say this happens every January,” he said. “In fact, many carriers do change the premiums throughout different periods of the year, so it’s not formally an annual notice of change.”

And like Medicare Advantage plans, Medigap plans are also very competitive, Oh said.

Plus, starting in 2024, Kentucky will join the six states that currently have a so-called “birthday rule” — California, Missouri, Massachusetts, Oregon, Illinois, and Louisiana. The “birthday rule” allows Medigap enrollees in those states to switch Medigap plans without medical underwriting during a period around their birthday. The birthday rule provides an annual open enrollment period where enrollees can switch to a plan with equal or lesser benefits, often at a lower premium.

Given that, Oh urges Medigap policyholders in those states to review their premium because they will vary across carriers even for the same plan.

Annual enrollment period

Now it’s not possible to review your 2024 plan against other offerings until the annual enrollment period begins in October. But once you’re able to compare plans, you should do so right away, experts say.

“It’s probably a good rule of thumb for Medicare beneficiaries to take the time to review their plan – whether Medicare Advantage or Part D – during the annual open enrollment period,” said Neuman. “And with so many Medicare plan options now available, it’s generally a good idea for beneficiaries to take a look at other available plans because they may find a plan that provides better coverage for lower costs.”

For more information

Read Medicare & You 2024 for more background about the ANOC, pages 63, 69 and 81. Medicare & You 2024 was not posted on Medicare’s website as of this writing. A CMS spokesperson noted that Medicare Advantage enrollees and Part D plan beneficiaries can also visit Medicare.gov for more information about the ANOC.