This post was originally published on this site

The 2023 rally by the S&P 500 index is being led by megacap tech-related stocks, whose weighting in the index is at a historically high level. That’s sparked a lot of worry about the durability of the bounce.

The S&P 500

SPX,

is up more than 7% so far in 2023, after last year’s 19.4% slide. The top 10 stocks hold a 29% weight in the index, and are responsible for around 70% of year-to-date performance, said Ross Mayfield, investment strategy analyst at Baird, in a Thursday note.

Within that top 10, seven of the leaders are “Big Tech” stocks, including the five largest, he observed, with Apple Inc.

AAPL,

and Microsoft Corp.

MSFT,

alone accounting for roughly 14% of the entire S&P 500.

Mayfield notes that this worries investors “because, typically, a ‘narrower’ market rally (i.e., fewer individual stocks rising) is seen as a sign of fragility and calls the rally’s staying power into question.” That could prove true, he wrote, but there’s also reason to believe it might not be a big deal.

Why is that? For one, unlike during the dot-com bubble of the late 1990s, the current crop of tech giants largely produce real earnings and strong cash flow, Mayfield said.

And second, concentrated leadership is far from unusual. In fact, it’s hard to avoid in an index that’s weighted according to market capitalization — the value of a company traded on the stock market, calculated by total shares outstanding multiplied by the share price. In a market-cap weighted index like the S&P 500, each component is weighted according to its market capitalization.

The structure is dynamic, Mayfield said, “rewarding recent winners, punishing recent losers, and ultimately reflecting the market’s momentum via its weighting.”

Over the last 40 years, the weight of the top 10 stocks in the S&P 500 has rarely been below 20%, Mayfield said. He acknowledged that the market today is more concentrated than that, which adds risk, but observed that only Microsoft and Apple are well outside the norm.

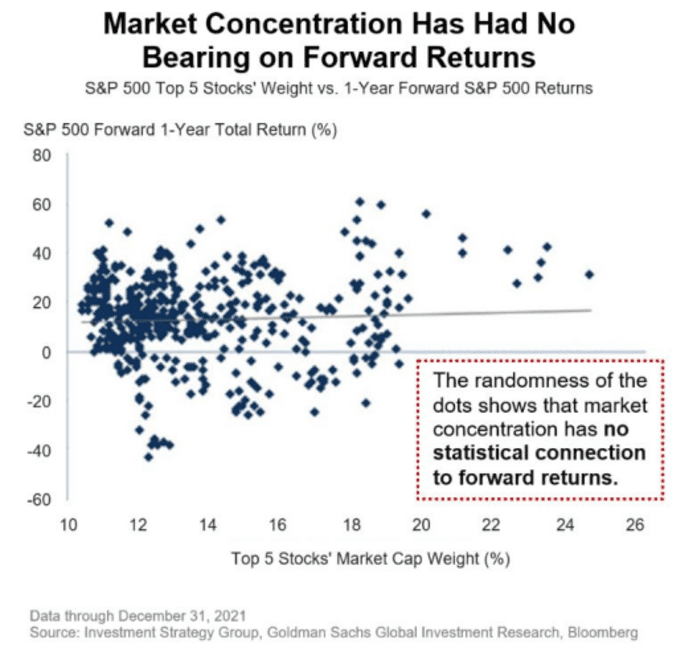

And what does a high level of concentration say about the future? Apparently, not much.

Investment Strategy Group, Goldman Sachs Investment Research, Bloomberg

“It’s not a useful indicator for forward returns,” Mayfield said, citing the chart above from Goldman Sachs, which shows that a high concentration at the top of the market doesn’t imply weaker future returns.

In fact, it doesn’t imply much at all, he said. “In a vacuum, more stocks joining a rally is healthier, but a top-heavy market alone doesn’t increase the risk of near-term underperformance.”