This post was originally published on this site

Why in the world would Republicans put out a plan to dramatically cut Social Security?

Even Donald Trump said he wouldn’t mess with the program’s benefits. Yet, the Republican Study Committee’s Blueprint to Save America, released in June, has a full section devoted to Social Security. I had never heard of the Republican Study Committee (RSC), but apparently the organization has served as the conservative caucus of House Republicans since its founding in 1973, and it currently consists of 158 of the 212 Republican House members.

Read: Yes, some Republican senators really are talking openly about Social Security cuts

If the Republicans take over the House, Rep. Kevin McCarthy has not ruled out cutting Social Security. So, it’s worth taking a look at what a Republican plan might look like.

The proposal in the RSC document — Make Social Security Solvent Again — is based on a bill put forward in 2016 by Sam Johnson (R-Texas). That legislation would eliminate Social Security’s 75-year deficit solely by cutting benefits. According to scoring by the Social Security actuaries at the time, the Johnson plan would reduce Social Security costs at the end of the 75-year projection period by 31%.

This 31% cut is the result of three major changes:

- Raising the Full Retirement Age—currently 67—to 69

- Dramatically reducing benefits for above-average earners

- Eliminating the cost-of-living adjustment (COLA) for individuals with income in excess of $85,000 ($170,000 for married couples) and using a chain-weighted inflation index for those below

Although the RSC takes a slightly different approach to raising the Full Retirement Age — linking it to increases in life expectancy — one would expect the overall impact on future workers to be roughly the same.

Read: Social Security COLA 2023 benefits are rising 8.7%—here’s what that means for recipients

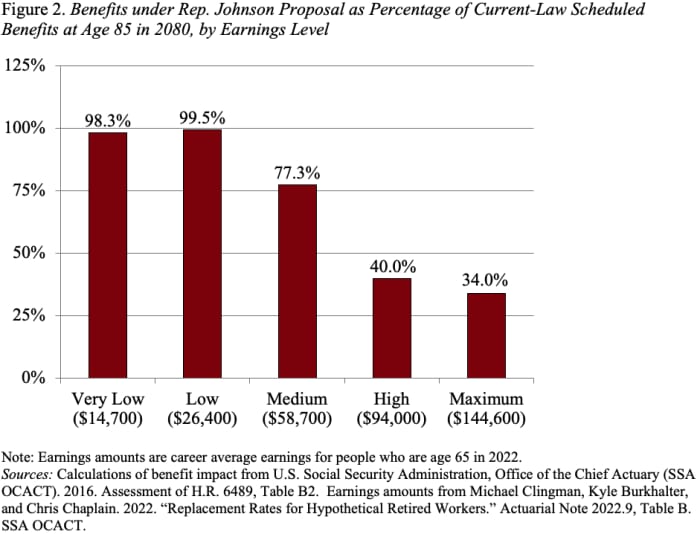

The best way to gauge the impact of these three changes is to examine the ratio of proposed to current benefits at different points in the earnings scale. Because the impact of eliminating the COLA increases over the retirement span, it is helpful to look at individuals at age 85. As Figure 2 below indicates, low earners are basically held harmless, while medium-earner benefits are cut to 77% of those provided under current law, higher earners to 40%, and maximum earners to 34%.

At first glance, one might conclude that’s a fine outcome: cut the benefits of the well paid and preserve the benefits of the low paid. But look closely at the earnings associated with the categories of well paid. The medium worker, who sees benefits drop to 77% of current law, had career average earnings of $58,700 in 2021 and the “high” earner, who sees benefits drop to 40% of current law, earned $94,000.

These are not rich people.

Read: Social Security’s COLA is no bonus

Moreover, changes to Social Security need to be made in the context of the entire retirement income system. Many households are likely to retire with little other than Social Security benefits, since at any moment in time less than half the private sector workforce participates in an employer-sponsored retirement plan. And among those lucky enough to have a 401(k) plan, balances are modest. The 2019 Survey of Consumer Finances, the latest comprehensive data available, shows that median 401(k)/IRA holdings of working households with a 401(k) approaching retirement (ages 55-64) were $144,000.

Policy makers do need to address Social Security’s long-run deficit, but the fact that a majority of House Republicans may support a plan that cuts Social Security by a third should terrify voters. Why put out such a document?