This post was originally published on this site

The Federal Reserve is speeding down the road looking in the rearview mirror, chasing a demon it doesn’t understand and praying that inflation will recede before it drives the economy into the ditch.

Almost every official at the Fed (with the possible exception of Vice Chair Lael Brainard) is fully committed to raising rates another 1 or 1.50 percentage point by the middle of next year unless they see clear signs of disinflation. But, as I’ll show, these Fed officials aren’t even looking for those signs.

I’m not the only one who worries that the Fed could be racing toward disaster if it raises interest rates FF00 too high. The biggest risk to the economy is that the Fed and other central banks will tighten too much, according to 55% of economists surveyed by the National Association of Business Economics.

Fed officials (and by extension everybody on the planet) have two big problems . One is that with its obsession about unemployment, wages, inflation expectations and sticky prices, the central bank is mistakenly concentrating on lagging indicators that will flash too late for it to avert a catastrophic recession or a financial crisis.

The second problem is that the Fed is looking at the wrong things anyway. The Fed’s model of inflation is inadequate at best, and fatally wrong at worst.

The Fed’s model

Let’s assume for a minute that the Fed’s model of inflation is correct.

The Fed’s current policy (based on the Expectations-Augmented Phillips Curve model) maintains that the unemployment rate is too low, which means that the supply of labor is so restricted that workers can demand (and get) higher wages and compel businesses to raise their prices in order to pay their wage bill. Once this wage-price dynamic is set in motion, everybody begins to expect higher inflation in the future and acts accordingly, creating a self-fulling prophecy.

To monitor their progress on bringing inflation back down to the 2% target, the Fed is monitoring the economic data, with a particular focus on wages, the unemployment rate, and the PCE and the consumer price indexes.

The problem is, these statistics are all lagging indicators. They tell us more about where we’ve been than where we are going. I’ve written before about why the CPI and the PCE price index will stay hot long after real-world inflation cools.

Read: Bernanke says Fed shouldn’t use interest rates to ‘fine-tune’ financial stability risks

Leading indicators

To see where inflation is going, it’s better to look at leading indicators of inflation, including commodity prices, house prices, supply times, the value of the dollar

BUXX,

DXY,

growth of the money supply, and financial conditions. Almost all of these have peaked and are now declining. That’s a sign that inflationary pressures are lessening.

If the Fed still wants a soft landing, it needs to heed these indicators. Unfortunately, the Fed, by looking into the rearview mirror, is not paying attention to the road ahead.

MarketWatch

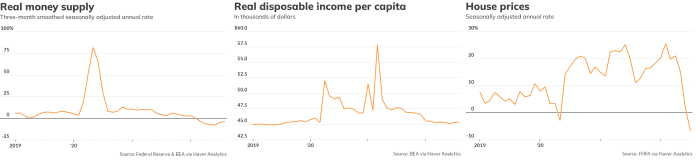

For instance, growth in the money supply has long been seen as a source of inflationary pressures. Larry Summers, Jason Furman and others who correctly predicted the 2021-22 inflationary cycle saw that large increases in stimulus (in the form of direct payments to households financed by the Fed’s quantitative easing) would lead to strong effective demand in an environment of restricted supply—a recipe for high inflation.

But that stimulus is now gone. Real disposable incomes are below pre-pandemic levels, and the Fed is shrinking its balance sheet.

The real money supply (adjusted for declining purchasing power) soared at a 66% annual rate in the second quarter of 2020 when the Fed and the Congress turned on the spigot of stimulus; it’s now falling at a 4% annual rate, the first sustained drop in the money supply since 2010.

Effective demand is softening, with real disposable incomes down 2.5% since the beginning of the year. Wealth, too, is dropping like a stone, with the S&P 500

SPX,

down 24% in 2022 and the Nasdaq Composite

COMP,

doing even worse. Higher mortgage rates have kneecapped the middle class’s wealth: their home. The stronger dollar is strengthening the deflationary forces from abroad.

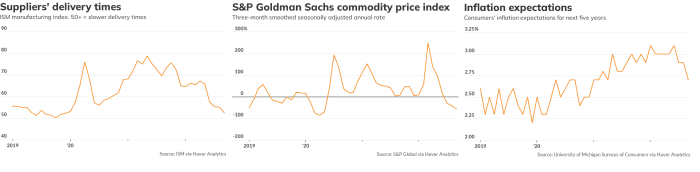

Supply is also adjusting. Delays in delivering prices are lessening and transportation bottlenecks are getting untangled.

MarketWatch

As the global economy begins to slow, commodity prices are falling, a sure sign that supply and demand are converging. The CRB spot index is falling at a 23% annual rate. Industrial metals prices are collapsing. The producer price index for intermediate goods is falling, and the PPI for intermediate services has decelerated.

Given the Fed’s obsession with wages and inflation expectations as the twin drivers of inflation, you’d think policy makers would be paying more attention to the recent deceleration in wages and to the reduction in medium-term inflation expectations.

Taken as a whole, these leading indicators of inflation point to a sharp deceleration in price growth. This is the soft landing the Fed is hoping for, but policy makers haven’t noticed.

Fed can’t explain inflation

The honest truth is that the Federal Reserve—like everybody else—can’t really explain inflation. Explanations that look good on paper don’t match the real-world experience very well. It’s almost as if economic relationship are complex networks that can change over time as people and their institutions change their behavior in unpredictable ways.

The Expectations-Augmented Phillips Curve Model is a nice story, but the evidence for this theory is thin. For one thing, the current bout of inflation we’re suffering from preceded any increase in wages or inflation expectations. The unemployment rate in 2019 was about the same as it is now — just under 4% — but inflation was slowing down, not speeding up.

Indeed, over the much of past 20 years, the correlation between unemployment and inflation has been negative, not positive, as the economy endured years of “jobless recoveries” and below-target inflation.

That’s why the Fed has had such a hard time hitting its inflation target. Even though monetary policy was very loose, inflation remained below target for most of the past decade. The Fed was stepping on the gas, but nothing happened.

Forget inflation: The loss of credibility is the true existential crisis of the moment for central bankers. They know they have to bring down inflation or their institutions will not survive in their current form.

They also know that the only sure way they know to do that is to crash the economy into the ditch.

Rex Nutting is a columnist for MarketWatch who’s been reporting and writing about economics for more than 25 years.

More opinions from Rex Nutting

Stop misreading the Fed: It’s not getting cold feet about wrestling inflation to the ground