This post was originally published on this site

Rallies are getting squashed and no lead appears to be safe for the stock market in recent trade.

In fact, the Nasdaq Composite

COMP,

intraday reversal on Thursday — when it was up 2.1% at its peak but ended down 1.3% — represented its largest reversal for a loss since April 7, 2020, according to Dow Jones Market Data. The Dow Jones Industrial Average

DJIA,

and the S&P 500 index

SPX,

which also were trading higher, finished in negative territory as well.

The disintegration of a big intraday uptrend comes after the Nasdaq Composite entered a correction — defined as a decline of at least 10% (but no more than 20%) from a recent peak — for the first time since March 8, 2021, and reflects the fragility of the market as it braces for a regime of higher interest rates and overall less-accommodative policy from the Federal Reserve.

History shows, however, that the intraday turnaround doesn’t appear to be a good sign for the market’s near-term prospects.

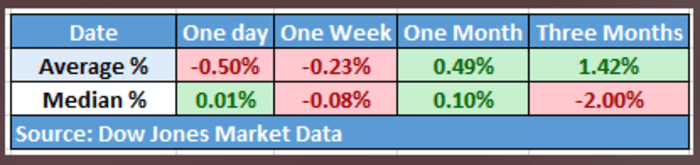

Based on days in which the Nasdaq Composite has registered an intraday gain of at least 2% but ended lower, the index tends to perform poorly.

On average, on such occasions, the composite finishes lower by 0.5% in the following session, and is down 0.2% a week later.

It isn’t until we get out a few months before performance improves. Gains for the index 30 days out are better, a gain of 0.5%, while three months out the return improves to a rise of 1.4%, based on Dow Jones Market Data, tracking 2% intraday moves going back to 1991.

Dow Jones Market Data

So things may turn around eventually.

But to put the move for the Nasdaq Composite into perspective, the last time it rose 2% and fell at least by 1% was March 20, 2020, the day before the so-called pandemic bottom.

See: At least 7 signs show how the stock market is breaking down

The equity market has been under siege at least partly because of the prospect of multiple interest-rate increases from the Fed, which meets Tuesday and Wednesday. Higher rates can have a chilling effect on investments in speculative segments of the market that rely heavily on borrowing, with investors discounting future cash flows. Talk of inflation also has put a damper on the market and is one of the key reasons compelling the Fed to change from a regime of easy-money to one of policy tightening.