This post was originally published on this site

Everyone’s talking about stagflation but no one on Wall Street believes it’s coming.

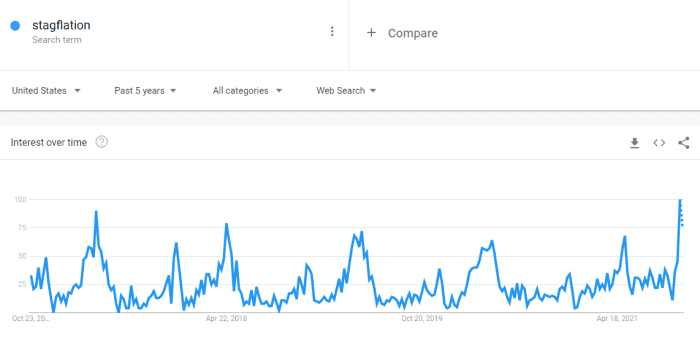

Google searches for stagflation

A sampling. UBS: “We don’t expect stagflation to become endemic.” Citi: “Stagflation is a metaphor (for now).” Barclays, on the prospect of European stagflation: “Talk of stagflation seems off the mark, as we expect HICP to drop below the ECB’s target in the third quarter of 2022.”

Analysts at Goldman Sachs also don’t think stagflation’s coming. BUT.

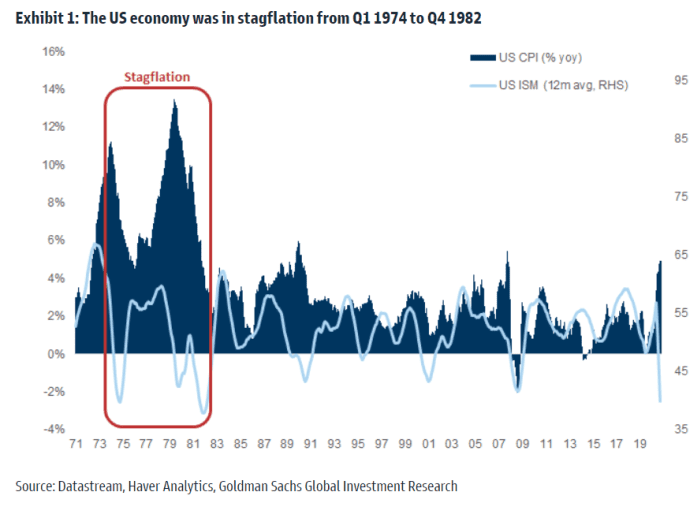

Strategists led by Lilia Peytavin looked at what happened in the 1970s to offer portfolio strategy advice during stagflation. They said the U.S. economy was in stagflation from the first quarter of 1974 to the fourth quarter of 1982.

In the U.S., the inflation-adjusted return was 0%, though U.K. equities delivered an 8% return (in part because U.K. stocks started to fall in 1973). Gold was by far the best asset to own, and equities outperformed bonds.

Sector-wise, however, there were mixed results. Real estate was the best-performing sector in the U.S., but there was a collapse in property prices in the U.K. as credit conditions tightened. “The experience of the 1970s illustrates that micro fundamentals often overcome the macro environment: a similar rise in interest rates created a downturn in the U.K. property market while real estate was the best performing sector in the U.S.,” they said.

Value outperformed growth in the U.S., but not the U.K. Energy stocks outperformed in both countries, and defensives outperformed cyclicals in both countries.

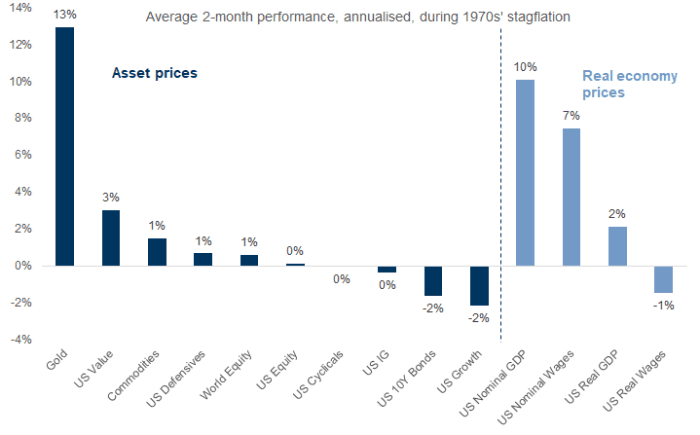

The chart

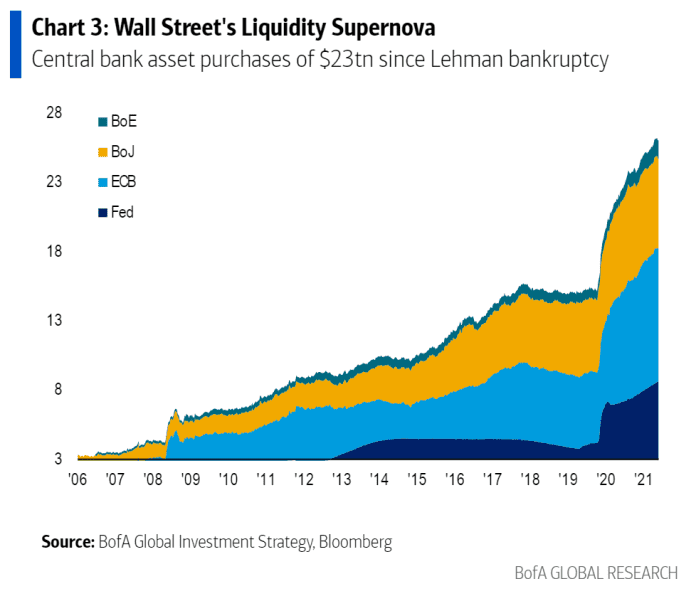

Turkey’s rate cut announced Thursday was the 1,000th globally since the demise of Lehman Brothers, according to Bank of America. They said the rate cuts are indicative of a “liquidity supernova” that is set to end next year. If 2020 was a growth shock and 2021 was an inflation shock, 2022 will be a rates shock, strategists led by Michael Hartnett said, which will be good for volatility and the U.S. dollar and bad for credit, stocks and tech.

The buzz

Snap

SNAP,

shares fell 20% and other companies reliant on internet advertising including Alphabet

GOOGL,

Facebook

FB,

and Twitter

TWTR,

reeled after the company’s fourth-quarter revenue estimate fell short of estimates, in what the company blamed mostly on the impact of Apple’s

AAPL,

new privacy settings but also global supply-chain woes denting the desire for corporate advertising.

Intel

INTC,

shares slipped as the chip maker beat earnings estimates but forecast slowing margins as it invests in building capacity and new technology. Toy maker Mattel

MAT,

rallied 7% after it forecast a strong holiday season.

Digital World Acquisition Corp.

DWAC,

the special-purpose acquisition company planning to merge with former President Donald Trump’s new media venture, surged above $70 in premarket trade, from below $10 before the deal was announced.

Federal Reserve Chair Jerome Powell has the last word before the quiet period ahead of the next Federal Open Market Committee meeting, with a speech at 11 a.m. Eastern on post-COVID policy changes. Flash U.S. purchasing managers indexes come shortly after the open.

President Joe Biden appears to have conceded that he doesn’t have the votes to increase corporate taxes. The U.S. Treasury is due to show how much red ink the country spilled in the September-ending fiscal year; the Congressional Budget Office, which usually gets it close, said the federal deficit was $2.77 trillion, down from the $3.13 trillion deficit in fiscal 2020.

Listen to the Best New Ideas in Money podcast.

The market

The Nasdaq-100 contract

NQ00,

saw particular pressure on worries over internet advertising, though the S&P

ES00,

contract was steady.

Gold

GC00,

was trading below $1,800 an ounce as the yield on the 10-year Treasury

TMUBMUSD10Y,

rose to 1.68%.

Random reads

Actor Alec Baldwin killed the cinematographer of the Western movie he was producing after discharging a prop firearm, authorities say.

So many elephants were killed for their ivory that now a large number have evolved to be naturally tuskless.

Need to Know starts early and is updated until the opening bell, but sign up here to get it delivered once to your email box. The emailed version will be sent out at about 7:30 a.m. Eastern.

Want more for the day ahead? Sign up for The Barron’s Daily, a morning briefing for investors, including exclusive commentary from Barron’s and MarketWatch writers.