This post was originally published on this site

October looms large in U.S. stock market lore. Yet there’s only one way the month lives up to its outsized reputation: It really is particularly volatile.

Before I summarize the historical data supporting this reputation, let me first dispel two Wall Street stories about October that turn out to be myths.

Myth #1: October is the month with the most major trend changes

This is simply not true. According to the bull and bear market calendar back to 1900 maintained by Ned Davis Research, nine changes to the U.S. market’s major trend occurred in October. September comes in higher with 10, while November is tied with October at nine.

The average number of trend changes across all months is between six and seven. None of these three months’ totals differs from the average to a statistically significant extent.

The source of this myth may be a related belief that October is a so-called “bear killer.” It is true that an above-average number of bear markets in the Ned Davis Research calendar did come to an end during October: eight, versus an all-month average of between three and four. But this historical factoid sheds no light on the U.S. stock market in October of this year, unless you think stocks are already in a bear market.

To be sure, the stock market could nevertheless experience a trend change this October. But if it does, it won’t be because it is the 10th month of the year.

This is important to keep in mind because it’s human nature to ascribe meaning to random events. For example, I argued a month ago that there was no good reason to expect September to be a bad month for the U.S. market. My argument still stands, even though the month did turn out to be rough for stocks, with the S&P 500

SPX,

shedding 4.8%.

If I told you that there’s no reason to expect a coin flip to come up heads, you wouldn’t conclude I was wrong even if the coin nevertheless did produce a heads. The same principle applies here.

Myth #2: October is the end of the 6-month seasonally unfavorable period

Actually this isn’t totally a myth. It’s just true in only one of every four years, and 2021 is not one of them.

I’m referring to the famous six-months-on, six-months-off seasonal pattern that goes by the names “Sell In May and Go Away” and the “Halloween Indicator.” As I’ve written before, this pattern’s statistical support traces to the third year of the so-called presidential election year cycle.

The third year of the presidential cycle so dominates the “Sell In May and Go Away” pattern that, upon focusing only on the other three years, there is no statistically significant difference between the average May-through-October and November-through-April returns. The underlying data is summarized in the table below, based on the Dow Jones Industrial Average

DJIA,

back to its creation in 1896.

| Average November-through-April return | Average May-through-October return | Difference in returns is significant at the 95% confidence level | |

| All years | 5.3% | 1.9% | Yes |

| Third years of presidential cycle | 10.7% | 0.0% | Yes |

| First, second and fourth years of presidential cycle | 3.6% | 2.5% | No |

Keep this in mind this month when you hear investment advisers trying to pinpoint the day in October in which it is best to jump the gun on the official beginning of the seasonally-favorable period — Halloween. In reality, because there is no seasonal pattern beginning in November, there is nothing to get a jump on.

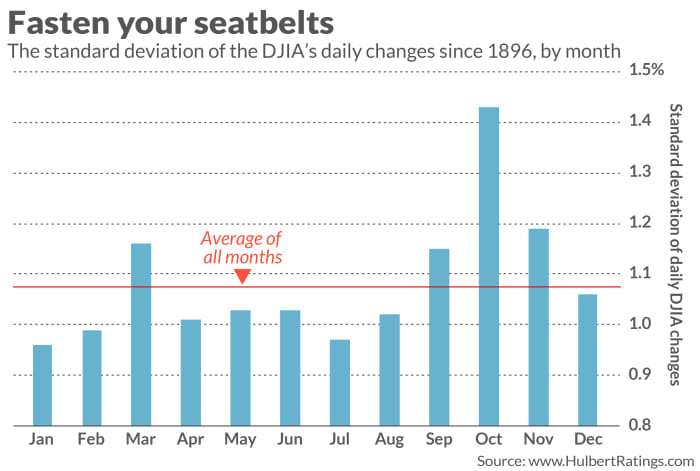

October is a particularly volatile month for stocks

Having dispensed with these two myths, we can focus on what is true about October: It’s he most volatile month of the calendar, as you can see from the chart below:

Unlike what we found with the “Sell In May and Go Away” pattern, October’s above-average volatility isn’t a function of just one year of the presidential cycle. It’s also been consistent: If we halve the period since the Dow’s creation, October turns out to be the most volatile in both the first- and second halves. Furthermore, the month remains at the top of the volatility rankings even if we remove 1929 and 1987 from the sample — the years in which the two worst crashes in stock market history occurred, both in October.

I’m not aware of any theoretical explanation for why October should be so volatile, and would normally recommend ignoring any pattern for which such an explanation is missing. But because higher volatility can be caused by nothing more than the expectation of higher volatility, there’s a good possibility that October’s reputation for volatility may persist.

There are a couple of investment takeaways. The first is not to let yourself be spooked by the increased volatility. Hold on tight and don’t get thrown off of your investment strategy.

Second, for those of you with a high appetite for risk, might be to take a position in one or more of the exchange-traded funds that rise when volatility spikes. The one with the greatest assets under management is the iPath S&P 500 VIX Short-Term Futures ETN

VXX,

Note carefully that this product (and other exchange-traded products that profit from volatility) is suitable for very short-term trades only, since these investments lose a small amount every day even when volatility stays constant.

Mark Hulbert is a regular contributor to MarketWatch. His Hulbert Ratings tracks investment newsletters that pay a flat fee to be audited. He can be reached at mark@hulbertratings.com

Plus: The S&P 500’s energy sector was the only port in a raging September storm for stocks