This post was originally published on this site

Stock-market valuations are “historically extreme” by almost every measure. And while valuation corrections don’t necessarily result in market pullbacks, the risk of a “hard” correction is growing, warned a top Wall Street strategist.

“With the current cycle advancing very quickly, the risk that the correction is hard is growing,” wrote Binky Chadha, chief strategist at Deutsche Bank, in a Thursday note.

The warning comes as Wall Street firms have expressed nervousness as equities continue to rally, pushing major indexes to all-time highs, without any significant pullbacks. Including Friday, the S&P 500 has gone 214 trading days without a 5% pullback, rising more than 33% over that stretch. That’s the longest run without a pullback since a 404-day run that ended on Feb. 2, 2018, according to Dow Jones Market Data.

Need to Know: This Wall Street firm is sticking to its S&P 500 price target. Here’s why it says a correction is overdue.

Major indexes were on track to lose ground for the week Friday, with the S&P 500

SPX,

and Dow Jones Industrial Average

DJIA,

threatening to extend a losing streak to five sessions. The S&P 500 is down just 1.7% from a record close hit on Sept. 2 and has more than doubled from its March 2020 pandemic low.

Chadha noted that while equities are “very expensive,” that fact alone doesn’t require a large market correction. That’s because valuations can fall if rising stock prices are outpaced by earnings growth, shrinking the price-to-earnings ratio even as share prices rise.

Those types of soft valuation corrections are typically seen early in a recovery when earnings growth is rapid, he said. During this recovery, however, the “compression” in earnings multiples has been slow and uneven, Chadha observed.

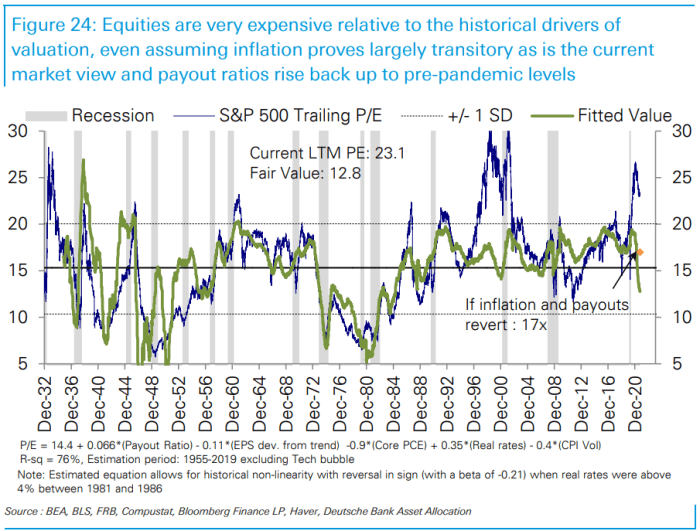

Using trailing 12-month earnings, the price-to-earnings, or P/E, ratio for the S&P 500 moved from a low of 14 at the depths of the pandemic 27 at the start of 2021. It has subsequently compressed to 23.1, a decline of 14%, as earnings outpaced the rise in prices, but remains 15% above its historical range of 10 to 20, he noted.

Deutsche Bank

Multiples based on forward earnings estimates have been going sideways at an elevated level. Other ratios, such as enterprise value, or EV, relative to EBIT (earnings before interest and taxes) and EV/EBITDA (earnings before interest, taxes, depreciation and amortization) are down modestly from record highs but remain above their tech bubble peaks, Chadha said, while cash-flow based valuations have continued to rise.

Chadha said a “surprisingly rapid rebound” in earnings is the most likely explanation for the extreme valuations, noting that S&P 500 earnings have topped the bottom-up analyst consensus estimate by an unprecedented 15 to 20 percentage points for five consecutive quarters. But that dynamic appears set to end, he said, noting the analyst consensus appears to have caught up, while the pace of earnings beats and upgrades, a key driver of equity upside, is set to slow.

“At a fundamental level, we believe the key reason multiples are high is market confusion over where we are in the earnings cycle, in part reflecting the speed and surprise with which the economic recovery has unfolded and the large persistent beats this generated,” he wrote.

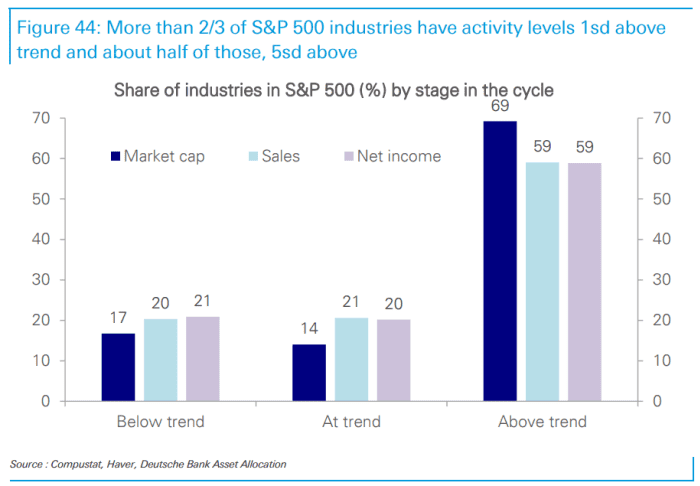

And since gross domestic product is still well below trend, there is a popular view that the best of the recovery has yet to come, Chadha said. The problem is that the parts of the economy that S&P 500 companies are most exposed to are already significantly above trend, he said, with 2/3 of S&P 500 industry groups showing activity levels that are one standard deviation or more above trend (see chart below).

Deutsche Bank

“So the cycle is much more advanced and the risk is that activity begins to slow, while the market is priced for most of the recovery as yet to come and large beats to continue,” he said.