This post was originally published on this site

Ellie R., 24, of Los Angeles, was brimming with hope for the future when she graduated from college in 2019. She landed a job at a financial startup and hoped to apply to law school — but in March 2020, the pandemic derailed her plan to take the exam.

“All my future plans were kind of put on standstill, and I was just put on survivor mode,” she said. “Everything kind of just crumbled.”

Because her parents were furloughed from their jobs and putting any income toward mortgage payments, Ellie sent them roughly $800 a month between March and December to help with utilities, phone bills and groceries. She eventually found it difficult to keep up with her own bills, falling behind on rent and phone payments.

“My check was now split into two — I had to pay my stuff on top of my parents’ stuff,” she said. She was unable to save the money from her stimulus checks, she added, and while she was grateful to secure renters assistance from the city, “even that came very late” and didn’t cover as much as she had expected.

Ellie’s parents have since gone back to work on altered schedules, with her mother concerned about job security and her father stretched thin due to an understaffed team. Ellie has been able to start saving small amounts and is gearing up again to apply to law school, but worries about “repeating the cycle” if there is another wave of COVID-19 shutdowns.

“My mental health hasn’t been great,” she said. “I’ve been really sad about all of it, and I get really anxious money-wise because I don’t know whether things are going to shut down again.” She says the one expense she made sure to maintain was therapy, which helped her through this time.

Ellie, who at 24 sits on the cusp of a generational cutoff and says she identifies most as a millennial, is one of many Latino Americans who have experienced the pandemic’s financial fallout — struggling to save even as they extend support to family members.

Those challenges and more were laid bare in a new Bank of America

BAC,

study shared exclusively with MarketWatch, which highlights contrasts in savings, emergency funds, financial responsibility for loved ones, and post-pandemic financial goals between Hispanic and non-Hispanic millennials.

Hispanic millennials are more likely than their non-Hispanic counterparts to say they didn’t have enough savings to withstand the impacts of the pandemic (27% vs. 17%) and to report that the pandemic had affected their ability to save (72% vs. 59%), according to the survey. They’re also more likely to still find it difficult to save (38% vs. 29%) and to say they don’t have a financial role model or someone to ask for financial advice (51% vs. 39%).

Some of the top barriers to achieving financial goals cited by respondents: reduced income (26%), inability to save (25%) and job instability or loss (19%). Hispanic millennials (19%) are more likely than their non-Hispanic peers (14%) to remain unemployed during the pandemic.

Bank of America

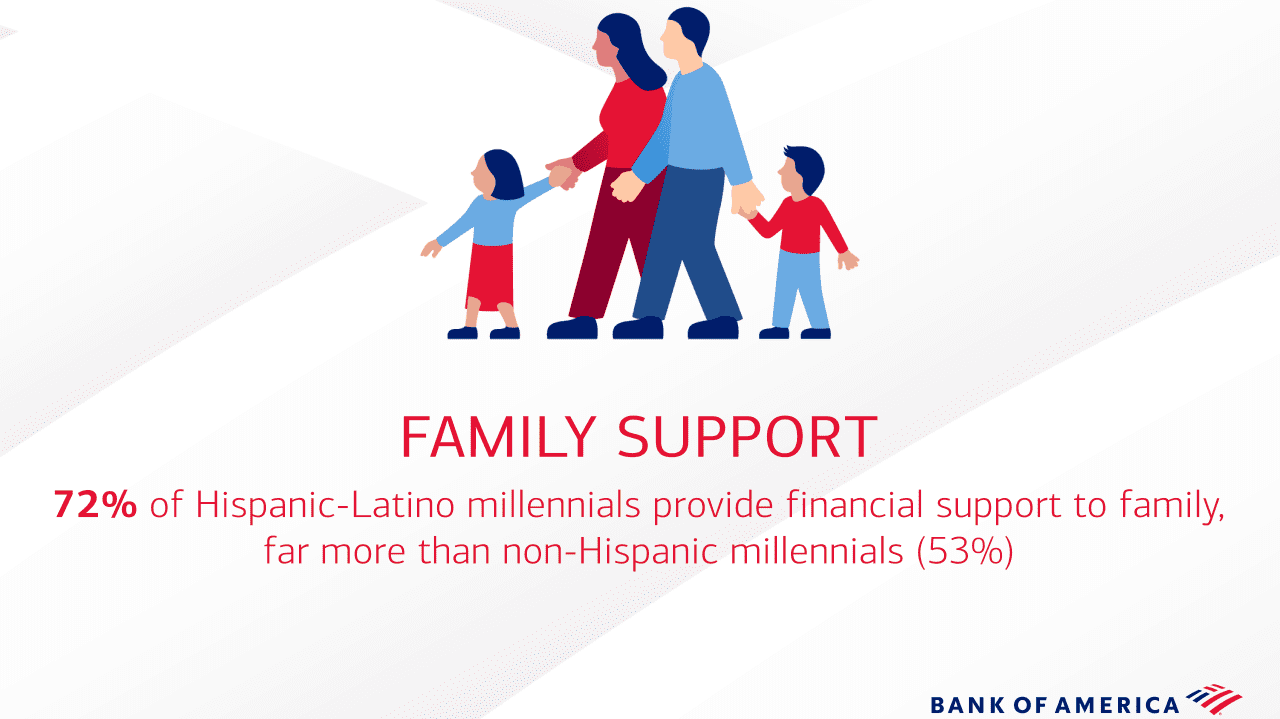

Meanwhile, about seven in 10 Hispanic millennials provide financial support to family members, compared to 53% of non-Hispanic millennials, the study found. Nearly a quarter say they’ve increased or are increasing their financial support for family due to COVID-19, with Hispanic millennials twice as likely (18% vs. 9%) to feel a sense of financial responsibility for their loved ones.

“The survey does reinforce the importance that family plays in the lives of Hispanic millennials,” Raquel Gonzalez, a Bank of America executive of Hispanic-Latino strategy for consumer and small business, told MarketWatch. “What we’ve seen is that commitment to family and their family’s wellbeing has only become stronger.”

Almost six in 10 Hispanic millennials are getting some kind of financial support from family, versus nearly half of their non-Hispanic counterparts, suggesting that “support is a two-way street,” the study added.

With that said, many respondents don’t appear to have “a financial role model or anyone they can really rely on for financial advice,” Gonzalez added, underscoring the need for financial education as Hispanic millennials continue to weather the pandemic’s impacts. She offered a plug for Bank of America’s Better Money Habits platform, which provides tools and resources in English and Spanish to help with goals such as saving, homeownership and retirement.

Tracking with national trends that show the pandemic-era caregiving burden has fallen disproportionately to women, Hispanic millennial women (56%) are more likely than their male counterparts (34%) to shoulder some kind of caregiving responsibility, the survey also found — and much more likely to be juggling work alongside child care (35% vs. 15%).

Hispanic millennial women who took on greater caregiving responsibilities were more likely than men to report financial challenges like decreased earnings or trouble paying bills.

Ellie, who did not take part in the Bank of America survey, had to take in her siblings for a month and a half after her parents contracted the coronavirus and had to quarantine. “I was basically being the parent of my parents, and being the parent of my siblings,” she said. “It was just a lot for me.”

“

‘I get really anxious money-wise because I don’t know whether things are going to shut down again.’

”

Ellie added that first-generation Latino Americans often feel a burden to be the “savior” of their family: “the one who first goes to college, gets the first corporate job, first everything.”

“In the moment, it feels nice because you’re the first one to do it,” she said. “But at the same time, no one ever considers the mental strain it [puts] on you, because you never feel like it’s enough.” The pandemic posed an unprecedented hurdle, she noted.

The survey of 1,015 general-population adults, 515 Hispanic adults and 394 Hispanic millennials (ages 24 to 40) was conducted by Ipsos between June 14 and June 28.

The study used the terms Hispanic and Latino interchangeably, with Ipsos employing an adapted version of a Census question to determine Hispanic ethnicity and asking respondents if they were Spanish, Hispanic or Latino. Respondents could self-identify as Mexican, Puerto Rican, Cuban and other Hispanic or Latino groups.

Plenty of previous data have borne out the pandemic’s disproportionate economic impact on people of color: A January study by Pew Research Center, for example, found that majorities of Black and Hispanic adults rated their personal financial situations negatively.

Why study Latino millennials in particular? According to Gonzalez, “they represent the future.”

“The Latino population tends to be younger, so we know the millennials will play a really important role in the workforce going forward, [and] their contributions to the overall economy will be important,” Gonzalez said. “In terms of the clients that we bank or those that we serve in our community, they will make up a strong percentage of the population.”

Hispanic millennials are also more likely to say that the pandemic has influenced their financial values or plans to spend or manage their finances (71% vs. 58% of non-Hispanic millennials), the study found. They’re more likely to say they plan to start an emergency fund after the pandemic (48% vs. 36%). Just over half say they’re “very” or “somewhat” optimistic about their financial outlook.

Ellie, for her part, is saving $20 per paycheck to build a financial cushion for future shutdowns. COVID-19 prompted her to reassess what’s worth investing in — she no longer feels the need for a gym membership or car, for example — and refocus her efforts on paying off her student loan debt.

The pandemic has also made her want to go back to school more than ever, as she seeks “a certain edge” to supplement her bachelor’s degree, citing Latinas’ well-documented wage gap compared to their non-Hispanic white male counterparts. She’s studying to take the LSAT this fall.

“It’s my dream that’s holding me together to keep fighting for it, because it’s still there and I still can obtain it,” she said. “That’s the one thing COVID took from me — I don’t want to let COVID take it again.”