This post was originally published on this site

PayPal and Square are well-known to investors as rapidly growing players in the payment-processing space. They don’t compete directly in all areas, but there are enough similarities to make a meaningful pairing.

Where PayPal and Square fit in

PayPal Holdings Inc.

PYPL,

was spun off from eBay Inc.

EBAY,

in July 2015. Square was founded in 2009 by CEO Jack Dorsey and James McKelvey Jr. (a current board member), and went public in November 2015. Dorsey also serves as CEO of Twitter Inc.

TWTR,

which he co-founded in 2006.

PayPal said in its 2020 10-K filing with the Securities and Exchange Commission that 13% of its revenue for the year came from customers on eBay’s Marketplace platform. It also said that no other revenue source represented more than 10% of the whole.

PayPal makes it easy to do payments online through its secure digital wallet — a user simply signs into their PayPal account to make a payment to the merchant from a bank account or credit card. The purchaser doesn’t need to provide any financial information to the merchant.

During 2020, 93% of PayPal’s revenue came from transactions, with the rest from “other value-added services,” a category that has declined over the past two full years.

Square offers what it calls a “cohesive commerce ecosystem,” which includes hardware and software, to help merchants process point-of-sale transactions and online transactions. Square also has Cash App, which helps individual users, businesses and organizations transfer money or bitcoin

BTCUSD,

through the app or by email.

“Customers can also use their stored funds to buy and sell bitcoin and equity investments within Cash App,” according to Square’s first-quarter 10-Q report (see page 42 of the report).

Here’s a comparison of quarterly and annual transaction volume for the two companies, with figures in millions:

(Company filings)

PayPal has a much larger payment-processing business than Square, and recently, its quarterly and annual transaction volumes have grown more rapidly.

Key metrics

Size, revenue and profit

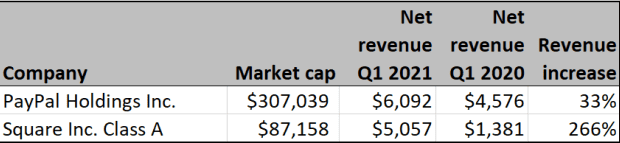

Here is a comparison of the companies’ market capitalizations and GAAP net revenue figures for the first quarters of 2021 and 2020:

(FactSet)

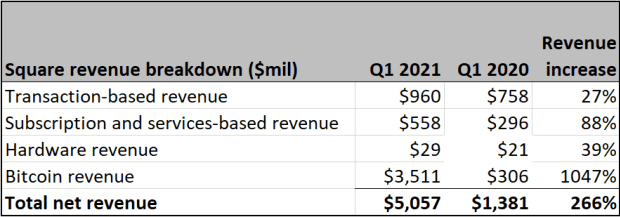

GAAP stands for Generally Accepted Accounting Principles, under which Square’s revenue from its bitcoin holdings has caused the company’s total revenue to balloon. Here’s Square’s more detailed revenue breakdown:

(Square shareholder letter)

This illustrates why an investor considering an individual stock has to take a closer look to form their own opinion.

Here’s what Square had to say about its revenue reporting in its first-quarter shareholder letter:

We deduct bitcoin revenue because our role is to facilitate customers’ access to bitcoin. When customers buy bitcoin through Cash App, we only apply a small margin to the market cost of bitcoin, which tends to be volatile and outside our control. Therefore, we believe bitcoin gross profit better reflects the economic benefits as well as our performance from these transactions.

More from Square’s shareholder letter:

While bitcoin revenue was $3.51 billion in the first quarter of 2021, up approximately 11x year over year, bitcoin gross profit was only $75 million, or approximately 2% of bitcoin revenue.

So Square’s adjusted net revenue for the first quarter was $1.55 billion, increasing 44% from the year-earlier quarter.

Excitement for bitcoin caused the spike in revenue for Square, as its Cash App users participated in the eightfold increase in the cryptocurrency’s price in dollars over the 12 months through March 31.

Here’s a comparison of gross profits (earnings before operating expenses) and operating profits (earnings before interest and taxes) for PayPal and Square for the first quarters of 2021 and 2020:

(FactSet)

PayPal has the larger payment-processing business, by far, while Square is growing its profits more quickly. Despite Square’s point that it derives a relatively small portion of its profits from bitcoin revenue, the massive amount of revenue from bitcoin transactions, including customers’ trades through Cash App, show the potential of this type of customer activity.

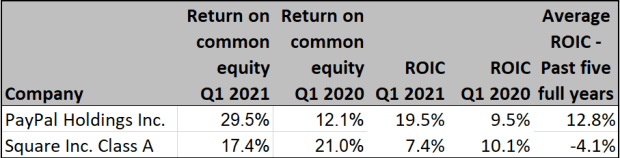

Returns on common equity and invested capital

These returns can give some insight into how well a management team deploys capital:

(FactSet)

Return on invested capital is earnings divided by combined debt and equity. It is a measure of capital allocation efficiency and can be useful when comparing companies that are similar. In this case, none of these numbers are bad — both companies are still growing their businesses in a dynamic environment.

Earnings estimates to 2025

Here are the actual earnings-per-share results for 2020 with consensus estimates among analysts polled by FactSet going out to 2025:

(FactSet)

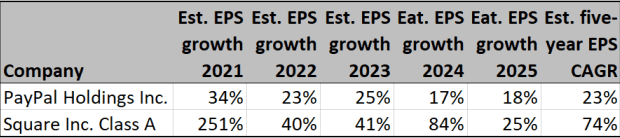

Here are estimated annual percentage increases in EPS based on the above, plus an estimated five-year compound annual growth rate (CAGR):

(FactSet)

That five-year CAGR for Square is bumped up by the expected EPS breakout in 2021. But if we run a four-year EPS CAGR from 2021 through 2025, the results are 21% for PayPal and 46% for Square. Both are impressive, but Square comes out on top if analysts’ estimates are close to accurate. This helps explain the much higher forward price-to-earnings ratio for Square that you can see further down.

Cash flow

In the modern economy, many investors believe free cash flow — remaining cash flow after planned capital expenditures — is a critically important measure. One reason for this is that so many one-time non-cash items can affect EPS. Another is that free cash flow can be deployed through business expansion, acquisitions, share buybacks dividends or other actions that will presumably be good for shareholders.

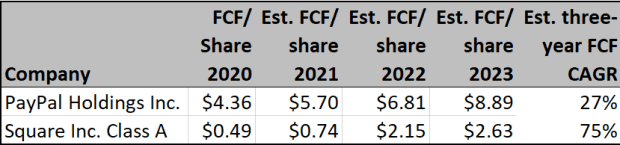

Square has had negative free cash flow (FCF) for two of the past four quarters, which isn’t surprising, as the company emphasizes growing its business. So it may be most useful to look ahead. FactSet has consensus estimates for FCF per share going out to 2023:

(FactSet)

Again, the analysts expect great things from both companies, especially Square.

Stock valuation and performance

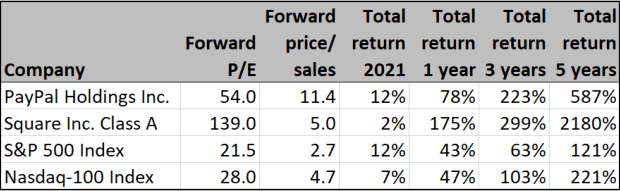

Here are forward price-to-earnings and price-to-sales ratios based on consensus estimates for the next 12 months, along with total return figures:

(FactSet)

Those are high valuations to expected earnings and sales. Then again, that has been par for the course for the most rapidly growing tech-oriented stocks over the past several years.

Wall Street’s opinion

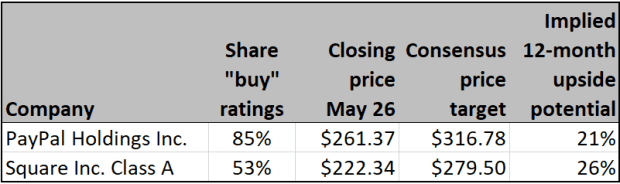

PayPal has more “buy” ratings among Wall Street analysts polled by FactSet, but Square as the more aggressive price target:

(FactSet)

Even though the analysts provide earnings estimates going many years out, their share-price targets are for 12 months, per tradition. This is where you need to think about what “long term” means to you as an investor. One year can be considered a short period for some long-term investors, who are looking to compound large gains over three- to five-year periods.