This post was originally published on this site

With broad stock indexes near record highs, investors are worried about pullbacks — and also about overpaying for new purchases.

Below is a list of companies whose forward price-to-earnings (P/E) ratios are low when you factor in how much they are expected to increase sales through 2023.

Rising P/E

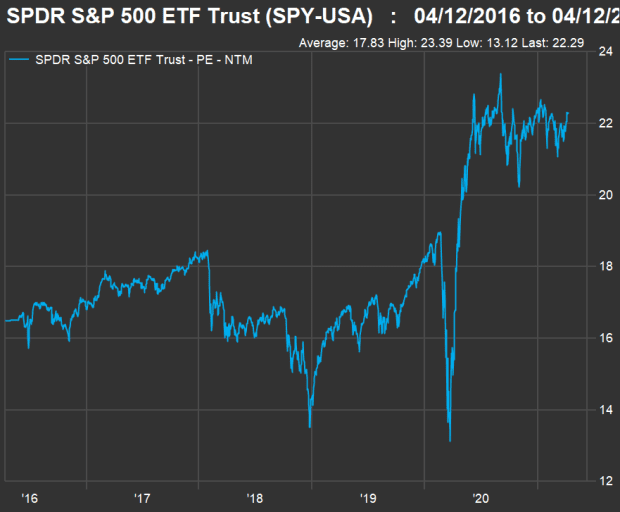

This chart shows how much the SPDR S&P 500 ETF Trust’s

SPY,

weighted aggregate forward price-to-earnings ratio has increased over the past five years:

(FactSet)

During this five-year period, the forward price-to-earnings ratio for SPY has expanded to 22.3 from 16.5, while the index has returned 120%.

Investors have placed a P/E premium on companies that increase sales very quickly. This doesn’t necessarily mean Amazon.com Inc.

AMZN,

is a bad stock to buy now, even though its forward P/E is 63.6, based on consensus estimates among analysts polled by FactSet. That’s down from 101.9 five years ago, and the stock has risen 461% in that span.

Here’s a look at stocks with high P/E ratios now, including Amazon and Netflix, that may turn out to appear cheap in retrospect several years from now because of their high expected sales-growth rates.

Fast sales growth expected

Following that screen, above, of “expensive stocks that might turn out to be great investments long-term,” here’s one that starts with the S&P 500

SPX,

and then looks at consensus estimates for sales per share going out to 2023. Since the pandemic has been so disrupted, our baseline for sales is calendar 2019 instead of last year.

A complete set of data for our screen, including consensus sales-per-share estimates through 2023, is available from FactSet for 458 companies.

We then pared the list to the 443 companies for which forward P/E ratios are available. (For example, United Airlines Holdings Inc.

UAL,

and Carnival Corp.

CCL,

are expected to post net losses for 2021, and you cannot divide by zero.)

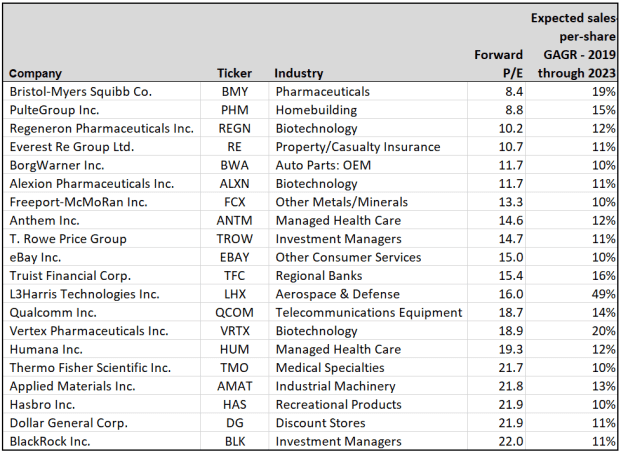

Here are the 20 remaining companies expected by analysts to increase sales at a compound annual growth rate (CAGGR) of at least 10% from 2019 through 2023, whose stocks trade at forward P/E ratios less than that of SPY (22.3):

(FactSet)

For the screen, sales per share was used rather than revenue, because the per-share numbers incorporate any expected dilution from the net issuance of shares. If the share count increases as new shares are created to award executives or fund acquisitions, for example, sales (and earnings) per share will decline. If the share count declines as a result of buybacks, the per-share numbers will increase.

It may be especially noteworthy during a housing boom to see PulteGroup Inc.

PHM,

a homebuilder, on the list. It is the second-least-expensive stock on the list on a forward P/E basis, following Bristol-Myers Squibb Co.

BMY,

How to find more information

The list is diverse and it is meant only to be a starting point for your own research. You can get much more information about each company, including ratings, price targets, news coverage and corporate profiles, by searching on its ticker on the top-right of this page.

One reason to do your own research is to understand a company’s business strategy, to help form your own opinion about its long-term prospects. Another is to gain further insight into why a company is expected to increase sales by so much. A company may be on the list as the result of a merger. One example is Truist Financial Corp.

TFC,

which was formed when BB&T acquired SunTrust late in 2019.

For Applied Materials Inc.

AMAT,

the industry description may be a bit deceptive. The company makes equipment and provides services and software for the semiconductor manufacturing industry, which is going through a period of high demand. It is included in the iShares PHLX Semiconductor ETF

SOXX,

and was on this recent list of semiconductor stocks favored by analysts.

Don’t miss: Dividend stocks are out of favor, but here are 19 that Wall Street loves