This post was originally published on this site

If you’re planning to take extra risk in your retirement accounts because of all the stimulus money about to be “poured into stocks”—don’t.

The same goes for bitcoin.

Mizuho Securities is the latest to push this idea, with a survey suggesting that 10% of the $380 billion in stimulus windfalls will be invested in stocks and bitcoin.

That, according to Wall Street, means that about $40 billion in extra money will “come into the stock market,” driving it higher.

Recently Deutsche Bank estimated young individual investors were ready to pour $170 billion into the market.

And the Wall Street hucksters made the same argument.

But it’s the old “money on the sidelines” fallacy. (Incidentally this raises, yet again, the question of why we don’t teach logic as Topic No. 1 in the public education system—a failure whose devastating costs are apparent every day.)

It’s a simple logical error, and it doesn’t matter who points it out—me, your broker, the Man in the Moon. It’s basic logic.

Stimulus money, or money “on the sidelines,” cannot “come into the market” for one very simple reason that gets ignored time and time and time again when this comes up.

Every time a security is bought, one must be sold.

Pretty obvious, right? If I buy your Apple AAPL, +2.27% stock, then you…er…have to sell it to me. I buy, you sell.

Read: These are the best new ideas in retirement

Imagine if you bought a house and tried to move in, and the previous owner figured he’d hang on to it, as well as banking the check.

If investors plunge $40 billion of their stimulus windfalls “into” stocks (and bitcoin), guess how much current investors will simultaneously “take out” of stocks (and bitcoin).

Er…$40 billion.

And if eager young investors rush out and pour $170 billion of their cash into these investments, current investors will…er…take $170 billion out.

It is not a coincidence that the figures match.

I have $10, you have a share. I buy your share. Now I have your share…and you have my $10.

None of this means the stock market is a bad investment (or a good one), merely that this particular argument has no force.

The more interesting question is whether or not this hot stimulus money will spark even greater animal spirits among investors — especially among those who have the least experience of investing.

Is that possible? Obviously.

Is it likely? Maybe.

On the other hand, $40 billion is about 0.07% of the value of the U.S. stocks market and $170 billion is 0.3%, so you have to wonder how much this additional euphoria is going to be worth.

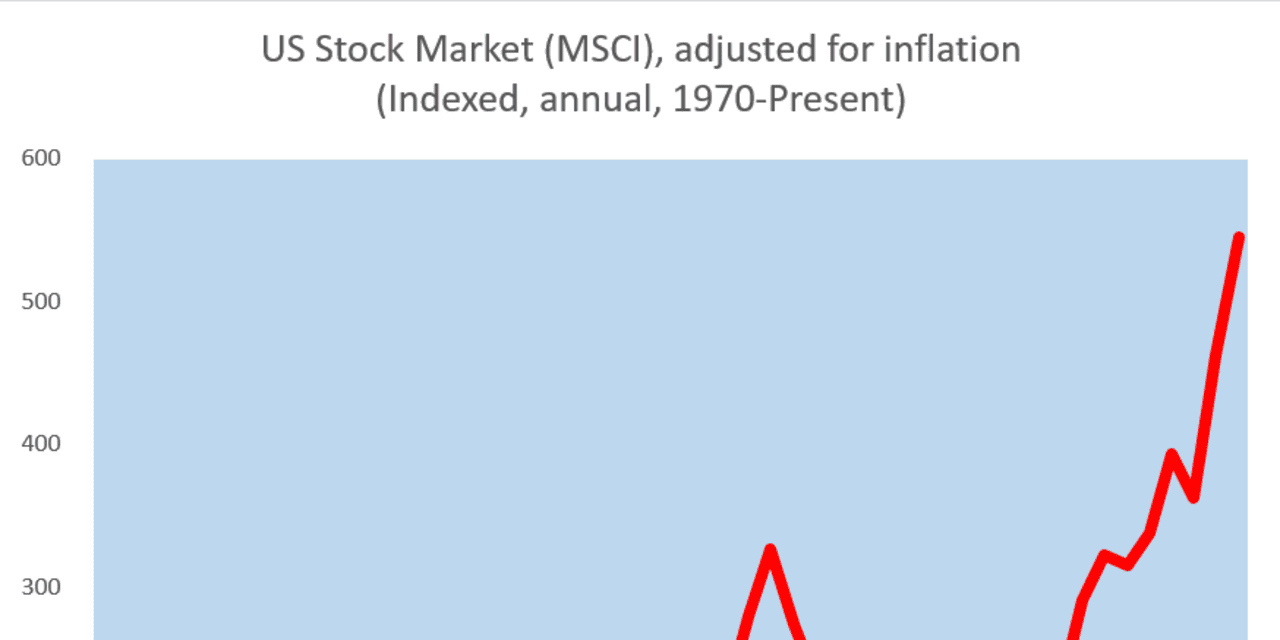

You might also reasonably wonder how much extra exuberance the market can handle, given — as the chart above shows — it looks pretty exuberant already.

For those following trends the more important short-term issue is that the U.S. market—as measured for example by the Vanguard Total Stock Market ETF VTI, -0.02% —is (just) above its 50-day moving average and well above its 200 day moving average. So the trend remains bullish.

Whether that remains the case as inflation forecasts break above 8-year highs, and the White House looks at a 25% hike in corporate tax rates, is going to be another matter.

Meanwhile those of a curious disposition might wonder why, if new and inexperienced investors are so eager to plunge $40 billion or even $170 billion “into” the market, current (and possibly more experienced) investors are so willing to take the same amount out.

Not sure if you can afford to retire? We can help you figure it out